Money is evolving in fundamental ways as technology enables new methods of creating and using it, changes that could potentially transform the financial system. Notwithstanding recent failures like the collapse of the FTX exchange, many cryptocurrencies have rebounded, banks are starting to turn cash deposits, bonds, and other instruments into digital tokens, and central banks are accelerating efforts to develop digital euros, yuan, and other currencies.

These innovations could build a future of money that’s safer and more accessible than what we have today, capable of making nearly instant payments across town or around the world at a fraction of the current cost. Leadership in this race is far from clear and circumstances could change significantly.

In a new paper, the Oliver Wyman Forum urges policymakers, bank bosses, and corporate leaders to consider several scenarios for how technology and policy may play out. They could revitalize the key role of banks and central banks in the creation and management of money, or fuel the rise of digital native firms or decentralized currencies and marketplaces where code is king. But change is coming that’s likely to shake up the financial order and transform the way we transact and invest — which is why companies and consumers need to pay attention too.

Digital ledger technology (DLT) like blockchain is driving these changes. It enables consumers, investors, companies, and others to make transactions directly using smart contracts rather than going through banks, brokers, and custodians. While many developers are working to make this happen, the winners won’t necessarily come from the world of Bitcoin. Banks and other incumbents are exploring ways of using DLT to turn deposits, bonds, stocks, and other assets into tokens, and trade them on their own platforms. And most of the world’s central banks are exploring or testing central bank digital currencies, or CBDCs, to maintain fiat money as the anchor of the global economy.

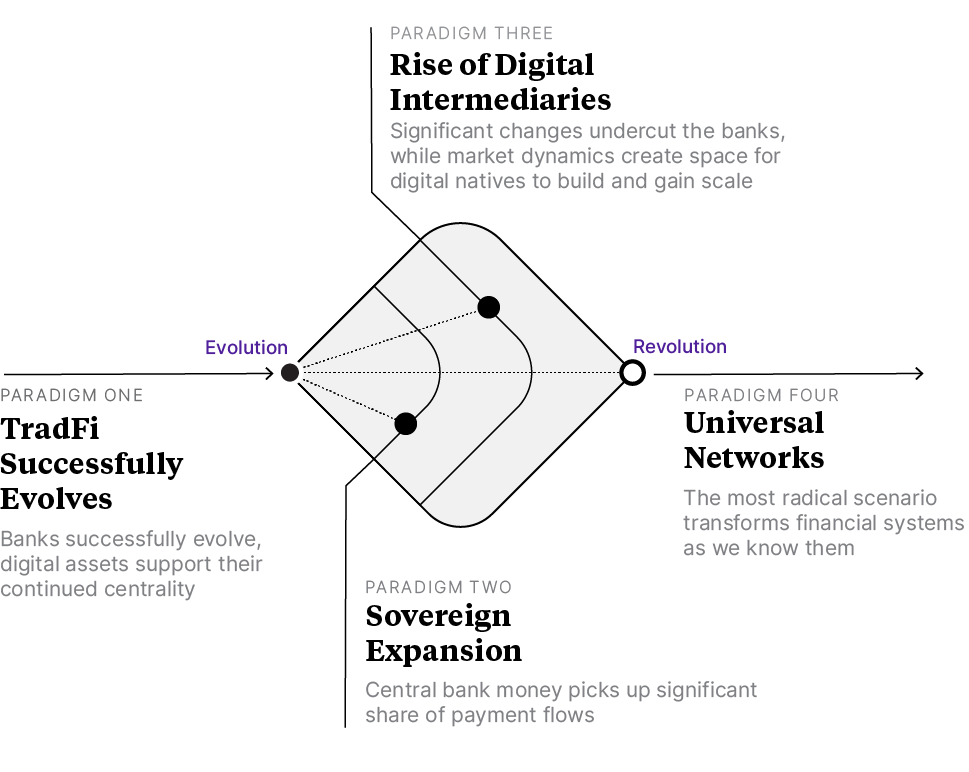

Here are four paradigms for the way money and markets could develop:

Traditional finance successfully evolves

Banks and other traditional financial institutions can also develop their own DLT-based solutions to tokenize both money and assets — an evolution of the current system, rather than a revolution. A recent paper co-authored by Oliver Wyman showed how three firms — Onyx by J.P. Morgan, Singapore’s DBS, and Japan’s SBI Digital Assets Holdings — carried out transactions involving tokenized deposits and tokenized government bonds on a public blockchain in an experiment under the Monetary Authority of Singapore’s Project Guardian.

Banks share the dilemma of many companies facing technological change: Do you disrupt your own business, with all the cost and uncertainty that entails, or wait and run the risk that an innovator takes the business away from you? But banks could benefit if authorities place new burdens on digital natives because of the failures of FTX and other crypto firms and favor traditional regulated entities.

Sovereign expansion

This scenario envisages governments and central banks embracing the new distributed technologies to create digital versions of their fiat currencies that capture a large share of payment flows. This vision is anything but far-fetched. More than 100 jurisdictions accounting for more than 90% of global economic activity are exploring CBDCs, including 11 that have launched digital currencies and another 18, including China, that are testing them in pilot projects, according to the Atlantic Council.

CBDCs haven’t gained critical mass in any of those countries yet. Governments in the exploratory camp have to decide whether CBDCs would be restricted for wholesale use, such as interbank payments, or made available to individuals widely, which might pose a threat to banks that control most consumers’ access to cash and credit today.

Rise of digital intermediaries

In this paradigm, which sits somewhere between evolution and revolution, nimble digital native firms gain scale with platforms that use fiat-backed stablecoins or tokenized deposits to drive everything from lending services to the issuance and trading of a wide range of digital assets.

With no limits from legacy technology or old-fashioned cultural norms, these firms could grow more quickly than established institutions and take customer relationships from them. Stablecoins were used in $7 trillion worth of financial transactions in 2022. But digital natives will need to win regulatory acceptance of their business models to gain substantial scale. The European Union’s new Markets in Crypto-Assets regulation, better known as MiCA, provides these actors the first framework for gaining such acceptance from a major economic actor.

Universal open networks

The most radical paradigm, this vision animates many cryptocurrency supporters. It would give rise to new open networks that enable borrowers and lenders, issuers and investors, and other participants to deal with each other directly, without intermediaries. Transactions would be powered by smart contracts and decentralized finance protocols, and algorithms could allocate credit, disrupting the business models of banks and digital natives alike.

Such dramatic change would most likely require a high degree of official support, and possibly new policy tools to take the place of the traditional regulated intermediaries that policymakers rely on to patrol financial markets today.

Which path, or paths?

These paradigms can clarify the issues and help banks, businesses, and policymakers as they consider their next steps. They aren’t mutually exclusive. Some, if not all, of these types of money are likely to play a growing role, depending on whether they are used for retail transactions at the corner store or to carry out multibillion-dollar cross-border trade deals or investments.

Institutions and policymakers should bear this in mind and seek to incorporate common standards and apply harmonized regulatory approaches to new forms of money and assets, and new business models. That’s the best way to define a future of money that works for all.

The old saw that investors would be well-served by selling in May and going away rings true this year. But they should make sure to buy a return ticket. The four-decade-old bull market still has life.

The Oliver Wyman Forum’s massive research project on the US equity market’s performance since 1871 shows that stock prices are driven by the ever-changing interaction between corporate profit margins, risk aversion, real risk-free interest rates, and society’s propensity to own financial assets. The market faces headwinds on all four of those drivers.

Profit margins are being squeezed by a slowdown in economic growth, a trend the regional banking crisis following the collapse of Silicon Valley Bank will amplify. The standoff in Washington over raising the US debt ceiling, which could trigger an unprecedented default, is likely to increase risk aversion and depress the market at least temporarily.

The latest interest-rate hike by the Federal Reserve underscores the central bank’s determination to win the battle against inflation. That suggests that real risk-free rates – already near a 10-year high – will remain elevated for some time. Finally, the US savings rate remains low as consumers spend down money set aside during the pandemic, which should curb demand for equities in the near term.

Those economic clouds make it more likely that equities will decline rather than rise, perhaps by 5% to 20%, in coming months. But that would be a typical cyclical setback, not a crash that might signal a secular bear market. The secular trend in corporate profits, one of the key drivers, remains strong because forces in the economy still favor capital over labor, as they have since the early 1980s. That’s likely to remain the case unless and until the democratic process tips the balance back toward workers

Vice President, Singapore's Economic Development Board

"You need to align private and public interests on a clearly defined common goal — something that is catalytic and ambitious."