Digital money and tokenization have the potential to transform the business of high-value flows. These big money transactions include large transfers between banks, payments by big corporations, and multi-billion dollar investments by companies, asset managers, and asset owners like pension and sovereign wealth funds.

Banks have long dominated this space, but tokenization will accelerate existing trends that have challenged bank business models. Distributed Ledger Technology (DLT) potentially enables computerized networks governed by smart contracts to enjoy the kind of trust that clients have historically placed exclusively in banks. The lines between payment and liquidity products blur as new competitors look to capture the best of both worlds, for example, by using tokenized money market funds to make payments. Technology will become more important than capital in providing a competitive edge as tokenization combines value and information. As tokenization takes off, bank business models will face further challenges from increasing competition by capital markets-based intermediation.

The impact and opportunity of tokenization will be significant. Tokenization could put at risk significant revenue for wholesale banks related to payments. At the same time, it would generate cost savings for the asset management industry given potential efficiencies in issuance and trading. Tokenization also can create even larger revenue opportunities from new products related to corporate balancesheet optimization and tokenization of real-world assets. For example, tokenization will facilitate the creation of new securitization products and could allow corporates to find better funding for working capital, creating revenue opportunities for the firms providing those products.

It is too early to tell how this competition between new and old monies will play out. Institutions managing large cash pools want safe sources of funds for transacting as well as for liquidity and collateral management. They need to trust that digital money has stable value and won’t lead to increased counterparty risk. That trust is hard to win and potentially easy to lose. Technological change is not enough. Policy and regulation for these new forms of money, and the types of companies that issue them, is still being determined and will have a major impact on the commercial viability of various models. While DLT-enabled capital markets can be trusted to move money across space, new market structures may be needed to ensure money retains its value over time.

In this paper, we present four visions for the way in which these technological and policy developments may transform the business of high-value flows, along with potential paths market participants can take to realize each vision.

The vision that's closest to the way the financial system works today would be one in which traditional financial institutions, or TradFi, evolve successfully by embracing DLT such as blockchain. That would require a radical change in the way banks, exchanges, and other financial institutions operate their middle and back offices, potentially bringing major efficiencies and cost savings, but it wouldn't involve a significant change in market structure. This scenario could increase the size and market share of today’s largest players or give smaller banks a lifeline, depending on how shared infrastructures evolve.

A different vision would see the rise of new digital intermediaries unencumbered by legacy technology who are able to provide investors and borrowers connectivity across various emerging networks. These digital natives could include asset managers who lean heavily on technology. Narrow money tokens like stablecoins, tokenized money market funds, and tokenized government securities could win significant market share. That would require a favorable regulatory environment and central bank support, so this scenario may be more likely in some jurisdictions than others.

Another scenario would see the rise of open universal networks, which use interoperable standards and protocols and allow the deployment of institutional-grade decentralized finance (DeFi) to permit competition among a wide variety of money issuers and digital solutions. Such models are already being tested in fintech sandboxes with official support in parts of the world. While it may take time for regulators to become comfortable with this approach, this paradigm would represent the culmination of a long-term trend toward capital markets-based financing, with money issuance mediated by smart contracts and protocols.

Finally, there is another scenario that would see sovereign governments take on a much more expansive role. While most governments and central banks that are studying or experimenting with central bank digital currencies (CBDCs) aren’t looking to fundamentally change their roles, crisis or politics may demand that change.

A replumbing of the financial system

Outlining the four visions for the evolution of the financial landscape.

The best way to predict the future is to build it. In the near term, we expect to see elements of all scenarios compete as policymakers flesh out regulatory frameworks and private sector players develop standards and forge new business models and relationships. While tokenization holds the promise of increased efficiency and a replumbing of the financial system in the long run, firms face pressure in the near term to identify additive and profitable use cases. Many solutions will find their path based upon industry, segment, and geography, as profitability of serving different types of clients will vary.

Firms should take a pragmatic and cooperative approach. As networks become more important, so does the importance of partnerships and industry forums. Firms should consider partnership models across scenarios to develop the appropriate capabilities, especially as the battle for talent will be fierce. Partnership models and ecosystem growth are crucial, not only to reduce costs but also to be able to scale solutions, as payments are typically just one leg of a broader set of transactions. Establishing the building blocks for tokenization is complex. Players who solve interoperability, scalability, standardization, trust, and privacy issues will have a significant advantage. Firms that participate in industry forums and public-private experiments will help identify new models and approaches.

Policymakers should prepare to innovate, adapt and be cognizant of the potential that new issuers and forms of money could pose risks to financial stability. Access to central bank accounts will be a critical enabler for secure digital money, while capital and liquidity requirements will significantly affect the feasibility of digital money initiatives. The policy environment will likely vary across jurisdictions, which could create tensions in global coordination efforts. Finding the right governance approaches will be critical to ensure financial stability with a technology that helps accelerate interconnectivity.

Our goal in this section is to illustrate from first principles the potential impact of digital money and tokenization on high-value flows and wholesale banking. We focus on what’s special about tokenization technology and how it solves market challenges differently from the traditional bank-based system. This will intensify competitive battlegrounds in wholesale banking, but in ways that are not entirely new. Tokenization and digital money accelerate ongoing transformations that have been shaping wholesale banking over the past few decades.

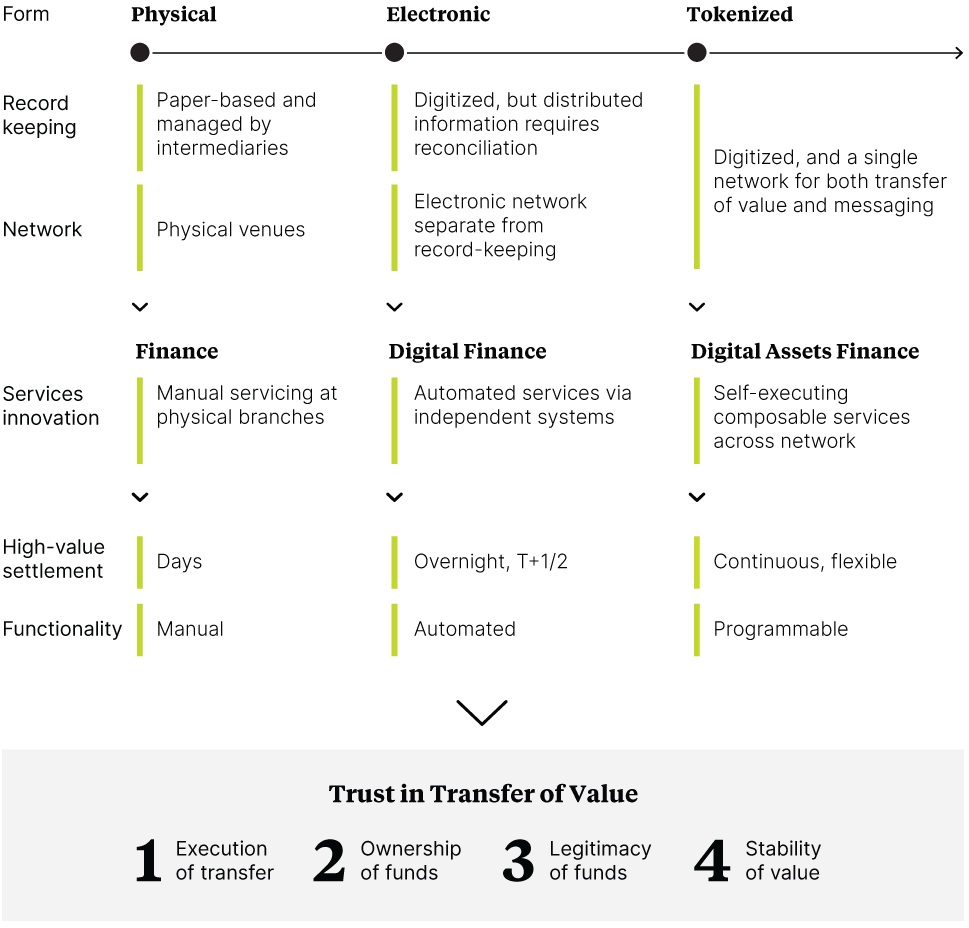

The financial industry has evolved to solve the challenge of transferring value between market participants. At the transaction level, this requires maintaining adequate records of who owns what and then correctly executing the transfers. Given potential concerns around money laundering and crime, there are also additional checks that funds are legitimate. On a macro scale, this also depends on a system that ensures value is maintained over time, as financial contracts can span years or even decades.

Evolution of Finance

Source: Adapted from “Institutional DeFi: The Next Generation of Finance?” by Oliver Wyman Forum, DBS, Onyx by JP Morgan, SBI Digital Asset Holdings; Assistant Governor Brad Jones “A Tokenised Future for the Australian Financial System?” Reserve Bank of Australia

The money that fuels the financial system comes from a two-tier system, with both the central bank and commercial banks playing distinct but vital roles in issuing money. Commercial banks combine money issuance with a number of different roles. They issue money when providing loans, which helps ensure that the growth of the money supply aligns with economic activity. The money they issue (deposits) is then used for payments, big and small. Banks maintain their own ledgers with records of ownership for clients and help transfer value, playing a role in both execution and compliance. This positioning allows banks to deepen client relationships and have the information needed to supply loans and other banking products. The central bank and the government, for their part, ensure that both public money, in the form of physical currency and reserves held by commercial banks at the central bank, and private money maintain “par value” — in other words, that a dollar issued by a commercial bank has the same value as one issued by the central bank. They accomplish this with a number of mechanisms including adjusting interest rates to control inflation, providing deposit insurance to ensure that a deposit from Bank A is worth the same as one from Bank B (a concept known as the singleness of money), and conducting interventions in times of crisis as the lender of last resort.

Technology has played a significant part in the evolution of this system. For centuries, the transfer of value involved the transfer of physical currency, a process that could take days if not months to execute. To provide people and businesses more immediate access to their funds, banks issued a series of money and credit products (including deposits, bank notes, and checks). New institutions like clearing houses emerged to support the networks of banks, allowing individuals and businesses to transact with commercial money while banks settled with each other using reserves. With settlement taking place after payments, this required banks to have not only access to these new networks but also capital to manage settlement risk.

Electronic money has enabled faster transfers but the need for trusted intermediaries remained. Digitization has expanded the ways in which individuals and businesses transact and how quickly those transactions are executed, but most assets remain in many separate ledgers and are traded in many different venues, including payment networks, clearinghouses, exchanges, and trading desks. This has meant significant complexity with various intermediaries needed to coordinate value transfer and messaging. On a global scale, institutions include messaging systems like SWIFT and cross-border settlement systems like CLS.

Tokenization is the next step in this evolution. It involves the creation of digital representations of financial or physical assets on a shared ledger such as a blockchain, where they can be programmatically managed and transferred. The tokenization process unifies the movement of value and information, allowing trust in intermediaries to be replaced by trust in networks. By synchronizing messages across a network of participants, the technology facilitates a process where everyone in the network can agree on the availability of funds. The key insight is that by providing a single ledger for all network participants to agree on, a verifiable message is the same as a transfer of value. Transactions can be settled with some immediacy without having to rely on any bank’s balance sheet.

The impact on competition will be significant. We expect that global banks could see cross-border payment revenue put at risk as demand for intermediary services drops and faster settlements slash the need for counterparties to deposit cash as collateral for their trades, cutting banks’ net interest income. We believe digital money and tokenization will reduce costs across the global securities industry, with the benefits shared by issuers, investors, and intermediaries when fully deployed. These savings would stem from blockchain technology’s ability to drive efficiencies in middle and back offices with straight-through processing for securities and derivatives transactions, as well as its potential to lower finance and compliance costs. As one party’s costs are another’s revenue, though, the industry also will take a hit to the top line. We believe these risks will be more than offset by new revenue opportunities from corporate balance sheet-optimization products and real-world asset tokenization services that banks can offer to wholesale clients. Companies today finance the majority of their working capital needs with retained earnings, a form of equity that’s relatively costly. Blockchain could enable companies to rely more on debt financing for their working capital by providing the transparency and immutability of data that financiers need to extend credit.

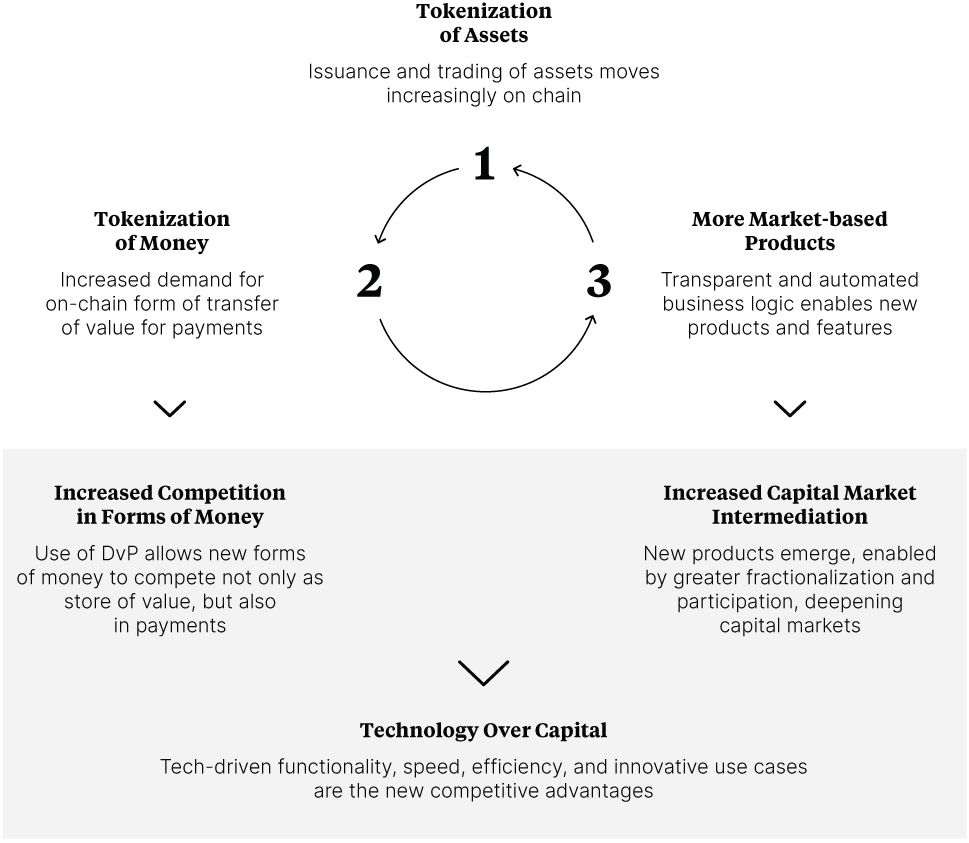

While that opportunity is up for grabs, tokenization will accelerate ongoing trends that call into question the role of banks in financial markets. The impact of tokenization depends on the amount of assets and liquidity being brought “on chain” (that is, onto shared ledgers). As assets are tokenized, the demand for digital money to trade these assets goes up, as does the utility of digital money for payments. With more tokenized assets and money on chain, the opportunity arises for more market-based products that leverage the unique advantages and programmability of shared ledgers. This flywheel effect increases the value of tokenization, attracting more assets on chain as institutional players take advantage of these novel products and services.

Supercharging Long-term Trends

Source: Oliver Wyman Forum

The growth of tokenization will generate increased competition for banks in forms of money and payments. Money market funds have been competing with bank deposits for years as a vehicle for storing value, but operational hurdles prevented their immediate use for payments. Now, money funds and similar instruments like short-term bond funds can be tokenized, fractionalized, and exchanged directly as payment tokens. Stablecoins, meanwhile, have proven the usefulness of digitally native money in crypto markets. As real-world assets are tokenized, these new forms of money will put at risk the fees and net interest income wholesale bank get from their payments business. Asset managers and tech firms, like digital custodians, will be able to facilitate cash management and provide liquidity services without relying on banks. These new firms can thus deepen the relationship with corporate treasurers,expanding opportunities to cross-sell.

Tokenization also will accelerate the growth of capital markets intermediation. The nonbank financial intermediation sector represents nearly 50% of global financial assets and its growth has outpaced banks in recent years. Increased competition in liquidity services opens the door to other profitable opportunities. Treasurers will have alternatives to operating accounts, allowing nonbanks to own the client relationship and offer bank-like products with capital sourced from the market. This shift will facilitate alternative funding avenues for hedge funds, letting them source liquidity from asset managers and private equity, who can create specialized funds for credit provision.

More digital money and expanded capital markets imply a third, less direct impact of tokenization: the ascendancy of technology over capital advantages as the key competitive advantage. Technology has already been changing capital markets, with alternative trading systems and highfrequency prop trading firms gaining market share from traditional dealers by investing heavily in data discovery and processing capabilities. Depending on the eventual structure of tokenized markets, on-chain data may become even more easily accessible, supercharging this competition. We have already seen the beginning of this competition play out on public blockchains with the rise of maximum extractable value (MEV) bots fiercely competing over transaction ordering. Treasury services in general can become far more automated as fintech players are empowered to compete and protocols can generate portfolios with specific risk-return profiles that CFOs need.

All these transformations depend on the ability of digital money to retain a stable value. Stability depends on liquidity management, as well as a variety of market and policy mechanisms. While on-chain settlement can rely on trust in the underlying network, liquidity driven crises can occur if there are disruptions in flow (and therefore net settlement) across different chains or between on- and off-chain markets, as we saw after the recent collapse of Silicon Valley Bank. Banks can access repo, interbank, and derivative markets to manage liquidity in normal times while central banks have tools like lender of last resort facilities to manage a crisis. Tokenization as a technology doesn't change the importance of preserving stability of value but changes what tools may be available (for example, more realtime data might allow early detection of impending crisis) and which ones may yet be lacking (for example, new money issuers may need access to liquidity mechanisms). Building appropriate liquidity management mechanisms is critical to ensure trust in the long run and will depend on both policy and action by market participants.

The transition may be slow until it is sudden. The size of tokenized assets today is small, at an estimated $6.5 billion in 2023. The market expects uptake of DLT for wholesale settlement in the next 5-10 years. But the flywheel effect of tokenization means liquidity can grow quickly once it takes off. There is a general consensus that tokenization will play a large role in the financial system by the end of the decade, with estimates for the amount of tokenized assets ranging from $4-14 trillion by 2030. This wide range underscores the fact that various outcomes are possible, influenced by policy decisions, technological advancements, and on-chain liquidity incentives. A window of opportunity has opened for new intermediaries and universal networks to challenge the prevailing dominance of commercial banks in private money creation.

The nature of future payment networks, the dominant forms of money, and ultimate winners in financial markets are far from clear. Ultimately, a reliable and safe digital money is necessary for tokenization to scale. Firms that hope to profit from a tokenized financial system with highly liquid on-chain capital markets must meet the demands of key users, principally corporate treasurers and asset managers and owners. These entities manage large cash pools and want safe instruments for transacting as well as liquidity and collateral management. They need to trust that digital money has stable value and that the payments process won’t involve greater counterparty risk than today’s methods. That trust is hard to win and easy to lose.

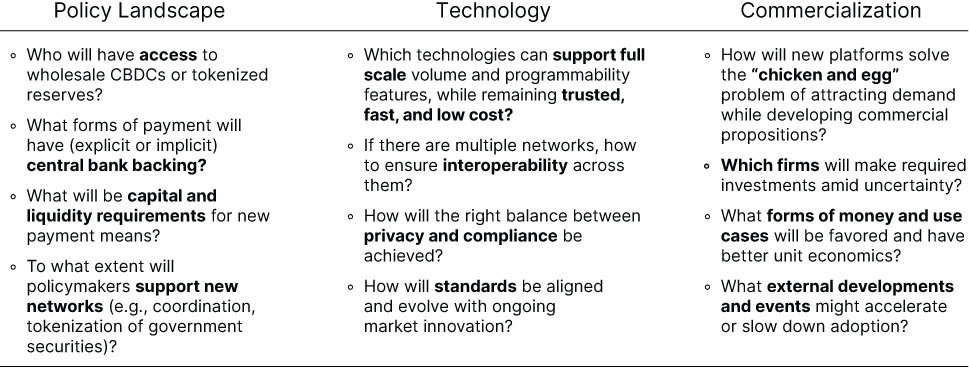

We see policy, technological innovation, and the development of a broad ecosystem as the three essential drivers of transformation, each with its own challenges. How stakeholders meet those challenges will define the future of money and which players prosper in that future.

Future of money drivers

Source: Oliver Wyman Forum

Central banks and policymakers play a fundamental role in maintaining trust and ensuring the integrity of the financial system. They oversee final settlement of payments, provide reserves for money creation, and manage credit conditions by adjusting interest rates. Moreover, their vigilant monitoring of financial entities and proactive stance against financial crises underpin confidence in the financial system. As digital money and tokenization reshape finance, policymakers see opportunities to modernize infrastructure, deepen capital markets, and bolster economic growth. However, this rapid evolution also presents challenges as it introduces new risks that may require new tools and policy frameworks. Policymakers may see reason to move slowly, balancing the drive to innovate with the need to carefully manage the transition.

One of the greatest concerns for central banks is ensuring “singleness of money,” that is, ensuring that different private money and public money trade at par. The system we have today in many ways emerged in response to crises where that singleness of money was lost. Many global and local regulations were designed to make banks safer, but digital money may increase financial activity and money creation outside of banks. Additionally, tokenization will increase the velocity of money and the potential interconnectivity between markets. Bearer money instruments such as stablecoins present their own challenges, as the price of the instrument is market-based, rather than established based on a bilateral relationship between issuer and holder. Central banks will need new tools, especially in a more capital markets mediated system where they can no longer rely on recapitalizing banks and may need to take on the role of “dealer of last resort.”

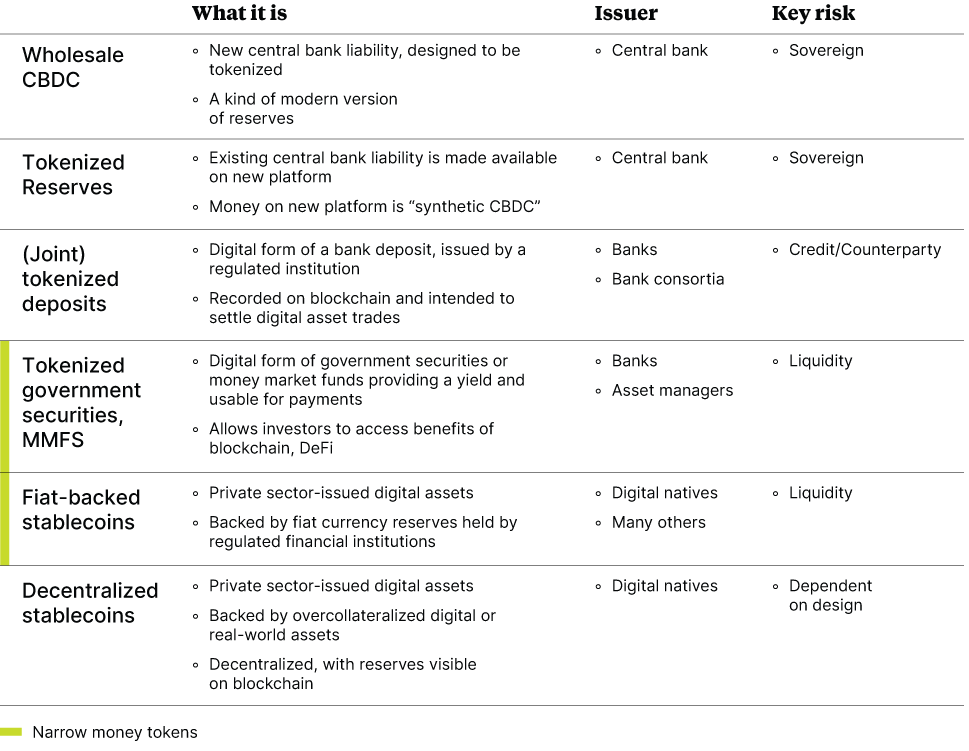

CBDCs are not the only option. While research on wholesale CBDCs has been advancing, with nine jurisdictions expecting to have a live one in service by 2030, central banks are also exploring alternative ways to tokenize central bank money (please see the image in the next page). An International Monetary Fund survey of central banks found that close to 80% of them either were not allowed to directly issue a digital currency under existing laws or the legal framework was unclear. But central banks could authorize regulated entities to issue tokens backed by reserves, which are central bank money. This solution would avoid the legal uncertainty around direct CBDC issuance and require only a suitable licensing regime for private issuers, along with rules on reserve requirements and the appropriate account structure for issuers at the central bank. There are different options for the account structure. The United Kingdom allows the Bank of England to create an omnibus account that enables providers to build a platform and operate segregated accounts for clients. The Bundesbank has tested a “trigger solution” that connects a DLT platform to the existing central bank real-time gross settlement (RTGS) system so activity on the platform “triggers” the cashleg settlement on the RTGS system.

Central banks are carefully considering who will have access to tokenized central bank money and on which platforms. Banks currently enjoy the privilege of central bank accounts, which is one major reason why private bank money today is fungible with reserve money. As emerging forms of money are able to bypass banks, that raises questions of whether new issuers also should also have access to central bank money and what is recognized as settlement. As trust in networks comes to rival trust in banks, central banks will need to choose between launching new networks or finding ways to connect emerging networks with existing platforms.

Policymakers will also shape the system by setting capital and liquidity requirements for new money tokens, as well as other risk management requirements. These mandates will affect the economics of different money tokens as well as their competitive edge and appeal relative to bank deposits. In December 2022, the Basel Committee on Banking Supervision set prudential standards for regulated institutions handling stablecoins, urging national regulators to adopt these by January 2025. However, alignment on tokenized deposits is still very early. The international harmonization of these standards will further influence the economic profiles of money tokens across different jurisdictions.

Tokenization of Central Bank Money

Source: Oliver Wyman Forum, adapted from publicly available sources

Policymakers can influence the pace of change through decisions related to the tokenization of government securities. Digitally native issuance of government securities could accelerate the growth of on-chain liquidity and support capital market development in some jurisdictions, especially if those securities are also used to back tokenized money issuance. The private sector has already begun the process of tokenizing treasuries, in a non-native manner, which carries its own risks.

Policymakers’ comfort with tokenization also will depend on how the technology shapes their own ability to serve their public mandate. Real-time data availability on the state of the economy could be transformative for both monetary and fiscal policy, expanding the tools available to assess the rates of growth and inflation and to interact with the public, for example, to distribute social benefits or collect taxes. Tokenization could also improve financial monitoring and supervision through regulatory technology, or RegTech. These approaches are still in their early days, with the European Commission putting out a tender to study decentralized finance (DeFi) for embedded supervision in Oct 2022.

There are many additional policy drivers. Legal developments will shape which forms of digital money are accepted by institutions and determine whether tokenized assets and transfers are recognized. Developments in taxation are also likely to have big implications for which solutions gain scale as corporations and investors adopt tax optimization strategies.

There are many technical challenges that must be overcome in order to unlock the full potential of tokenization. The strategies of all actors in the ecosystem, no matter their current or future role, will depend heavily on the ability to scale blockchaininspired financial infrastructure. This may occur on private networks, public networks, or a hybrid solution, but all participants will face the same technological trade-offs around security, scalability, and governance when building a new network. Combined with the need for privacy, interoperability and standards, there are many choices and uncertainties when building on programmable networks.

Security is a foundational element in financial infrastructure. Both the underlying networks and applications built on top of them must be designed to protect assets from attack in order for adoption to take off. Public and private chains approach security threats differently, but successful networks must ensure they do so while preserving credible neutrality, meaning the network is not biased in favor of any actor or group of actors.

Scalable networks need to offer low transaction costs and high throughput. Network transaction costs need to be kept low; otherwise, intermediaries will have an incentive to emerge and help internalize cost. Public chains face a trade-off in achieving security, scalability and decentralization simultaneously. Yet decentralized networks might offer greater network resiliency. With more participants, it is more likely a sufficient percentage of the network will be live to process transactions. Further, geographical decentralization helps ensure that nodes are resilient to data center outages, political interventions, and energy supply issues. Private chains can offer more tailored solutions to operational requirements, but they face more challenges in driving activity given constraints on participation.

These technical trade-offs mean that different actors will construct different kinds of networks depending on their needs, leading to a potentially siloed financial system. Achieving interoperability between these networks is crucial yet challenging, reminiscent of the more-than two-decade gap between the US Defense Department's launch of a decentralized communications network, ARPANET, and the inception of the World Wide Web. Until a fully functioning network-of-networks is established, there will be limitations on the free flow of liquidity, activity, and information. Progress is being made with application-specific blockchains, or “app chains,” that exist as separate networks but utilize shared settlement infrastructure. In the absence of complete technical solutions, though, intermediaries will inevitably surface to mediate the flow of value and information across networks.

Composability within networks is just as important as interoperability across networks and depends on participants' ability to collaborate effectively. Financial markets can unlock significant value when all involved parties can simultaneously access and act upon comprehensive information, derived from a shared, reliable source. This is particularly impactful in high-frequency transactions that depend on complex chains of sequential business communications. Areas where this is most beneficial include stock borrowing and lending, OTC derivative margin and lifecycle management, repo processing, and tri-party collateral management services. For business processes to unlock the value of composability, the information must be freely discoverable by other network participants, and there must be a shared environment for programmability.

Data sharing and discoverability will need to be balanced with privacy. Solutions will need to fine-tune the exact type and amount of data being shared, and with whom, to prevent the unwanted sharing of proprietary information. How and when to make necessary aspects of identity available generates complexity and cost in the current financial system. Ensuring the legal integrity of the system via Know-Your-Customer (KYC) and Anti-Money Laundering (AML) checks is critical, as is understanding your counterparty risk in any transaction. Progress here depends on the development of effective identity solutions, whether through decentralized, portable identities or the emergence of new trusted intermediaries.

Critically, the development of DLT technology and its potential application in financial markets requires common standards. Standards are imperative to ensure effective protocol integrations, cryptographic security, uniform data formats, verifiable identity mechanisms, streamlined tokenization processes, robust governance models, compliance with legal frameworks, secure custody solutions, stable network structures, and more. In the absence of common standards and interoperability, the value of tokenization may be limited, or captured within the walled gardens of intermediaries who succeed in gaining scale.

The utility of digital money for high-value payments depends on building liquidity within networks, creating a “chicken and "egg” problem. Firms need to attract users as they deploy new technology, but tokenization doesn't deliver the greatest benefits until it is applied throughout the value chain. That begs the question of which should come first: a network's" growth in users or the presence of a valuable assets within the network. As such, it is unclear whether banks or disruptors will win the race in making the investments and developing the right products to attract clients their assets on-chain. To capture the benefits of blockchain, banks will have to eventually replace their legacy systems — a time consuming and expensive proposition. DLT technology will reduce costs in the long run but tokenizing assets and issuing digital money requires firms to maintain both new and legacy systems for a transition period that could last years. Parts of the current infrastructure are quite optimized from a bank perspective, and we have heard in our interviews that senior management at many banks want a 10x use case to justify the upfront investment in new technology. As DLTbased experiments keep proliferating, banks must carefully consider which opportunities to pursue. When banks do act, though, they can leverage significant resources and relationships for big impact.

On the other hand, blockchain native firms may be quicker to market with innovations like programmable payments, but they start with little market share or track record, and being early is no guarantee of success. Their main advantage is seeing around the corner on emerging use cases, but their need to raise significant money to develop new products is a limiting factor, especially in today’s higher interest rate environment. In a 2022 survey of institutional investors, 63% of respondents said they were comfortable trading tokenized assets only with highly rated traditional institutions, while 47% stated they were precluded from working with digital native firms for custody. This has motivated some firms to consider tokenized treasuries and money market funds rather than stablecoins to align their products with existing legal frameworks.

Emerging Money Tokens

Source: Oliver Wyman Forum, adapted from publicly available sources

Economics of different forms of money matter. Investors and treasurers will be comparing both the yield and the risk profile across options when deciding what forms of money to hold. For issuers, the economics will depend heavily on the capital and liquidity legal requirements they face. Tokenized deposits are far closer to deposits under the current two-tier system and in theory should have a lower cost of funding relative to narrow money tokens. However, the opportunity cost for balance sheet optimization matters. Narrow money tokens will likely have a different capital requirement than tokenized deposits, and could be preferred depending on what regulatory requirements are most binding to the bank. As trust depends on stability of value, it remains to be seen what market mechanisms emerge to allow issuers to access liquidity and expand the money supply in response to changes in demand, especially when issuing narrow money tokens.

Commercialization strategies also will depend on the broader innovation environment. The potential impact of tokenization on treasury cash management is significant, not just for banks but for all corporations. Improved visibility and programmability can allow more proactive and forward-looking cash and liquidity management. As many treasuries have been streamlining back-office operations, they are likely to be increasingly dependent on new solutions to adapt to evolving risk management paradigms. The richness of the ecosystem may thus depend on how easy it is for these new solution providers to emerge.

External events, such as economic crises or regulatory changes, may play a pivotal role in commercialization models. Crises, in particular, have the power to swiftly alter priorities as individuals and institutions seek refuge from the source of those crises. Moreover, digital money is an ecosystem where success begets further success, and proven use cases drive increased liquidity. In this ever-evolving landscape, emerging technologies like AI and quantum computing hold both promise and challenge. While quantum computing has the potential to disrupt existing encryption methods, it also offers opportunities for creating even more robust security measures in the world of digital finance.

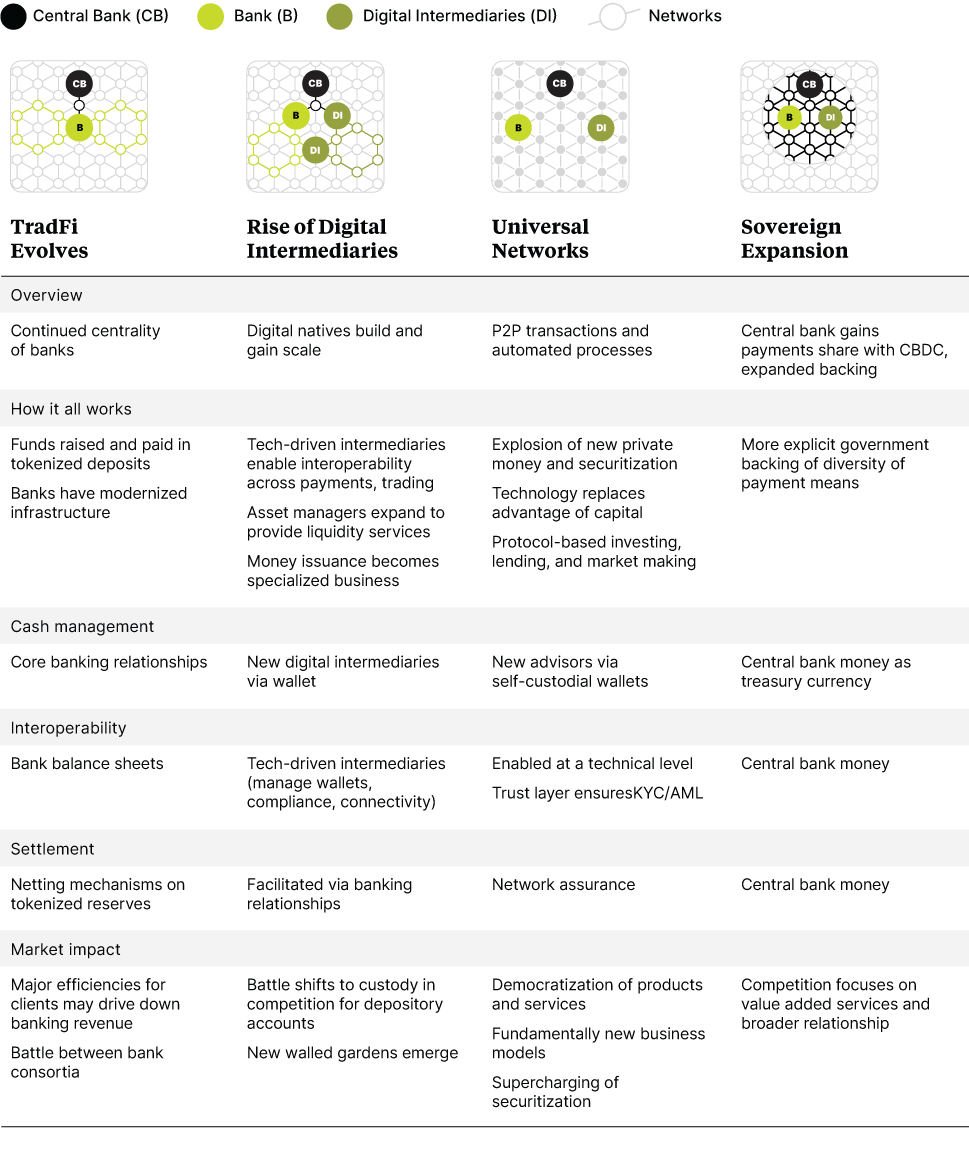

While digital money and tokenization may transform financial markets, it’s unclear who will drive this change and how the payments landscape will look when the dust settles. Will we simply swap out the technology and leave the incumbents in charge? Or will agile fintech players maximize the opportunity to change the status quo? Perhaps the cypher-punk vision of a decentralized financial ecosystem plays out. Then again, in a changing landscape, central banks may need to play a bigger role in financial markets. In this section we explore four visions for the way that digital money may change the world of high-value flows and wholesale banking. Each one imagines a substantially transformed system driven by different business models, something that could take a decade or two to play out. We expect to see development along all four paths, with the future system combining elements of multiple visions.

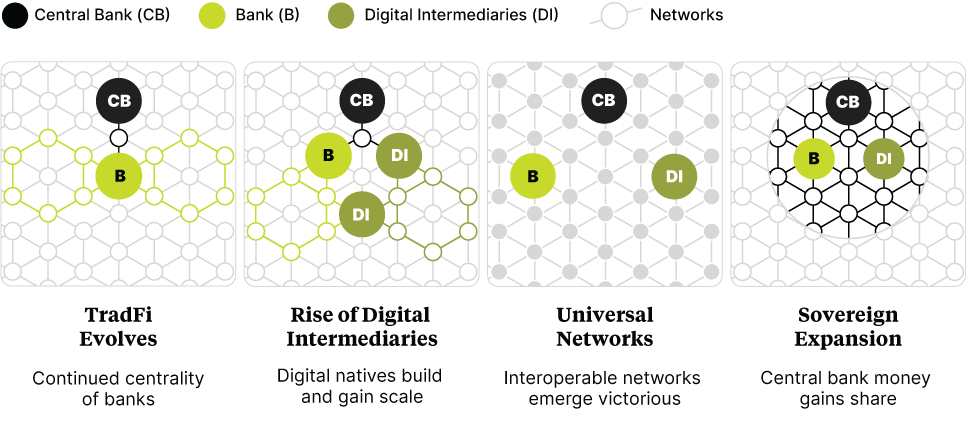

Comparison of Four Visions

TradFi Evolves

In this vision, traditional financial institutions continue to play the dominant role in high-value payments and the financial system more broadly. They adapt by embracing disruptive technology and successfully modernizing their infrastructure. Banking relationships also become more important than ever as banks provide critical advisory services to guide clients through accelerating changes in financial markets.

Overall, market structures remain largely intact, as banks are able to win the race to liquidity by leveraging their relationship networks and trust. Tokenized deposits replace demand deposits as liabilities on bank balance sheets as the increasing relevance of tokenization demands a digitally native form of money. Banks maintain their role in market making, especially for illiquid assets that are not easily tokenized. Treasurers continue to manage cash through core banking relationships, as bank-issued money tokens provide them the flexibility to streamline their back offices and adopt new risk management solutions.

In this vision, the two-tier system remains as tokenized deposits are linked to central bank money. There are a number of ways to achieve this, for example through wholesale CBDCs or tokenized reserves connected to legacy RTGS systems. Banks continue to enjoy exclusive access to central bank master accounts, although now using tokenization to improve settlement efficiency. Programmability improves coordination across parties, with benefits expanding to compliance.

As banks connect to multiple blockchain systems, their balance sheets serve as trusted bridges between private networks and different bank tokens, reinforcing their intermediary role across diverse market infrastructures and token types. Benefits from increased efficiency are passed onto bank clients, who are drawn not only to the assurance that bank money tokens can retain stable value relative to central bank money but also by their attractive economics.

Liquidity will shape which money tokens succeed. The relative liquidity of different money tokens will influence participants’ willingness to hold them. Digital money issued by larger institutions will have an advantage compared with those issued by smaller competitors given the counterparty risk. The blurring of lines between payment and liquidity vehicles could promote increased competition among banks leading in payments and those leading in asset management. This dynamic will foster a competitive race toward confidence, liquidity, and utility, with potentially winner-take-all dynamics leading to a handful of money tokens dominating unless mechanisms emerge to improve token interoperability and safety. Consortia also may offer joint deposit tokens, diversifying the counterparty risk of any single bank and increasing the liquidity of their payment tokens to compete with larger players.

Competition intensifies as banks and bank consortia race to bring activity to their preferred networks. Bank groups that successfully push their proprietary networks may open up new business models. For example, a bank-run network that provides DLT as a service could emerge, allowing any company to deploy their own subnetworks. Large banks that take an early lead in blockchain experimentation may have an edge, especially if they successfully open their platforms to other players to foster a more innovative ecosystem of products and services. However, it’s unlikely that one system will emerge as the sole winner, especially when looking internationally. Consortia-led networks directly linking banks together may prove dominant — and provide a lifeline to smaller banks struggling to compete.

Rise of Digital Intermediaries

This vision represents a regime change led by disruptors, not incumbents. Digital innovators succeed by translating tokenization into superior financial products for businesses, outperforming traditional banking services. These new intermediaries specialize in combining off-chain and onchain components to stitch together liquidity across networks as the foundation for useful applications.

In this paradigm, there are numerous financial networks that arise, both public and private. Interoperability is not achieved on a technical level but rather by new intermediaries who can manage cross-network custody, compliance, and connectivity on behalf of end users. By ensuring interoperability across networks and offering secure, reliable custody solutions, they deliver valued experiences that mask the underlying complexities. These intermediaries would tap into a vast array of applications on both public and private networks, curating the most beneficial products for their clients.

We expect an expansion of narrow money tokens such as stablecoins, tokenized money market funds, and tokenized treasuries. These instruments become the obvious choice for disruptors as they compete directly with traditional banks and their deposit token networks. Tokenized deposits may still play a role, but more and more products and services are accessed via capital markets, obviating the need to hold balances with a bank. For example, when large corporations need to borrow money, they can access funding and distribution services from new intermediaries that provide direct connectivity to blockchain-based capital market protocols.

We also anticipate that money issuance will become a specialized role. Narrow money token issuers that provide neutral infrastructure for digital disruptors will likely see widespread adoption of their tokens across numerous commercial use cases. Specialization in minting and technology allows for small teams that can operate with low expenses, making them especially profitable endeavors. But low headcount may imply outsourcing risk management to the market, and it’s an open question as to what types of controls should be put in place.

If regulation can be established and stablecoins reach a level of systemic importance in the financial system, the institutional framework could extend to include some central bank support for these issuers. This support could take various forms, such as access to an omnibus account at the central bank, effectively making stablecoins a form of synthetic CBDC or reserve-backed token. Stablecoin issuers are advocating for this access today.

This process leads to the commoditization of bank balance sheets and leaves banks primarily acting as dealers for collateral or supporting funding for market making. In this scenario, the battle may shift from maintaining operating accounts to providing enhanced custody solutions. As the primary relationship owner with institutions, these custodians will be in a strong position to sell additional products and services, further eating away at the traditional business of commercial banks. We already see leading crypto exchanges investing heavily in custody today and in new services liked secured lending.

These digital intermediaries could include an unlikely TradFi player: techdriven asset managers. Current crypto custody providers are tech companies that will resist adding advisory personnel, which would lower their operating margins. Asset managers are well positioned to step in to provide both advisory and liquidity services, such as access to money market funds or repos. Asset managers who are able to perform these services across the various network options will likely rely on a technology and informational edge. Stablecoin issuers also will compete with tokenized securities from stand-alone asset managers, providing a new form of yieldbearing digital money. Today, stablecoins issuers work hand-in-hand with asset managers, but that dynamic may change if they begin to issue competitive forms of private money.

Universal Networks

In this paradigm, open universal networks become the new infrastructure for financial markets. A highly interoperable set of networks (or even a single network) emerges victorious, with network effects winning out over any attempts to fragment liquidity. As finance becomes largely peerto- peer, protocols automate many of the functions that intermediaries play today. The permissionless nature of open platforms and the composable nature of their transaction software means that any entity can deploy, customize, and access financial products and services with relative ease.

These low barriers to entry will challenge traditional players to adapt or be replaced, as previous advantages that were provided by capital and large balance sheets will be replaced by advantages from cutting-edge technology. Banks and asset managers will be forced to invest heavily in new capabilities as on-chain data and information processing becomes a core competency across financial services.

Competition will eventually lead to most financial services and products offered by banks today being carved out and handled separately by specialized providers. Fundamentally new techbased business models would emerge to compete for the business of treasurers and asset managers, with technology winning out due to more discoverable information and composable business processes. For example, the classic function of the dealer may be replaced by automated market maker (AMM) protocols. High-frequency trading on-chain is already evolving as sophisticated bots identify, package, and submit arbitrage opportunities to specialized block-builders. Brokers are similarly replaced by specialized tech-driven entities that compete in Dutch auctions to fulfill orders on behalf of end users. New interfaces can then enable investors and corporates to access these solutions, with financial institutions potentially playing a role in helping vet and certify appropriate products.

This paradigm enables a kind of Cambrian explosion of money tokens and securitization products that are made easily available to corporations and investors. Treasurers and asset managers can design portfolios that meet the specific risk-reward trade-offs they seek. Digitally native yield bearing assets become widely available and easy to interact with through non-custodial wallets. New protocols could emerge to algorithmically package and distribute risk, while new interfaces would help scan and select options. New derivatives markets emerge on chain that can hedge risk into the future. The easy plug and play of financial solutions also could also allow corporates to offer their own financial products, through embedded finance or issuing their own money tokens.

A regulated trust layer would be needed to build confidence in the system. The future shape of on-chain identity and credentialing are far from clear, but a solution would reliably separate legitimate actors and businesses from the minority of bad actors on these open networks. Privacy solutions would need to evolve to a point where institutions and policymakers are comfortable that KYC and AML compliance requirements are met, while maintaining enough privacy to allow market participants to transact on-chain.

Policymakers may become comfortable with this approach because of its open competition, transparency, and new capabilities provided by real-time tracking of the economy. The expansion of composable protocols could lower the cost of participation and foster a long tail of financial products, increasing innovation and competition. Stability of value could be ensured by settlement with tokenized central bank money, which could be made accessible to institutions outside of banks that meet regulatory requirements. Central banks may choose to be interoperable with public networks or integrate directly by issuing reserves on public chains.

Sovereign Expansion

This scenario is characterized by an increased share of central bank money (or money explicitly and directly backed by the central bank). Across all prior visions, we imagine the balance between private and public money remains somewhat intact, with the potential share of private money increasing given new forms of money. In this vision, whether the central bank money reaches end users via banks, digital intermediaries, or directly on universal networks, far more flow is based off central bank money. It could be that money tokens are backed on a one-to-one basis with central bank money, making them a synthetic CBDC or tokenized reserves, or the central bank could issue wholesale CBDCs directly on a public, permissionless network.

A greater role for central bank money could also lead to greater unbundling between payment and money creation, as well as behavioral change. If CFOs are able to hold central bank money at scale, that could be the dominant form of money for operational cash while private money dominates precautionary and reserve cash. CFOs would be able to incorporate tokenized central bank money directly into their treasuries, eliminating any counterparty risk from private money. Payments would settle as soon as assets change hands, whether directly on universal networks or via custodians in a world with intermediaries. Competition in financial services would focus on value-added services and the broader relationship with clients.

Most central banks are not planning to dramatically alter the existing financial system. Yet as with any major transformation, the tokenization of the financial system could lead to unexpected outcomes. The most likely drivers of sovereign expansion would be either unintended failure leading to crisis or unintended success leading to increased political pressure to increase the remit of central bank digital money. As a result, implicit backing of private money may become explicit backing, and there could be an expansion of access to central bank money.

The role of the central bank will depend on the choices made in tokenizing central bank money. Some central banks may choose to foster a more level playing field through access to central bank money while others may prefer to provide a basic level of digital public infrastructure. Direct issuance of central bank money on private-sector controlled networks means the central bank will have to grapple with more questions around infrastructure governance than if central bank money were tokenized in central bank-owned platforms.

The use of digital money for high-value payments is still in its early stages. Tokenized deposits exist mainly in experimental form for supporting payments within a bank client network. While central bank experiments with wholesale CBDCs and tokenized reserves abound, none of these experiments have gone live. Stablecoins have reached scale but are limited mostly to trading within cryptomarkets. The demand for highvalue tokenized money is limited outside crypto given real world asset tokenization is also still in its infancy. The total digital bond issuance as of May 2023 amounted to approximately $3.3 billion, a minuscule fraction of the $127 trillion global fixedincome market.

The futures described in the preceding sections will not come about overnight. They will take shape incrementally, driven by the actions and innovations of industry leaders. This disparity between the current state and the envisioned future highlights the challenges and complexities of transitioning to a new financial paradigm. This section lays out possible paths to get from where we are today to each of the four possible futures of money.

Adoption Paths

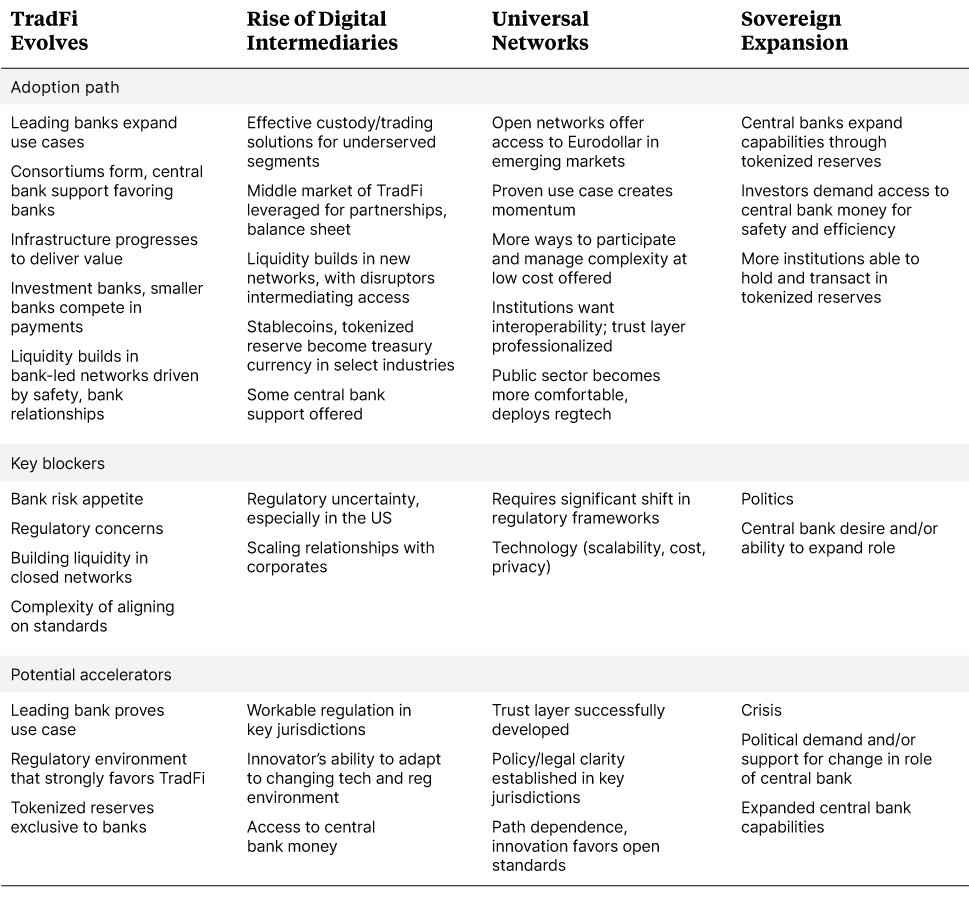

TradFi Evolves

Financial institutions have begun to prepare for tokenized money, with early use cases emerging within walled gardens and intrabank settings. These pioneers are transacting real value for clients but scale is limited. Interbank experiments are also underway, although at even earlier stages of development. No interbank projects have been fully launched but their backers’ ambitious goals hint at what could be possible if banks seriously invest in interoperable blockchain networks. The TradFi Evolves paradigm depends on the success of these various experiments.

Potential tailwinds include banks’ strong commercial networks and the degree of trust they enjoy among institutions. Most corporate clients and investors are more interested in having access to products that add value rather than championing specific technologies. Participation could be driven by slashing unit costs and proven commercial use cases such as delivery versus payment (DvP), a settlement method that delivers securities to a specified recipient only when payment is made. At the same time, banks without a strong presence in payments today, such as investment banks and smaller banks, may compete by forming consortia and building a tokenization proposition for asset managers, where they have strong relationships. Over time, as liquidity builds in bank-led networks, market participants could increasingly value the safety of these networks over public permissionless chains while continuing to derive value from bank advisory relationships.

As the financial landscape gradually adopts tokenization and tokenized deposits, opportunities arise to redesign settlement infrastructure, enhancing products with realtime data and efficient flow that are evident in automated trade finance and streamlined compliance processes. This transition brings systemic benefits, encouraging policymakers to adapt regulations to the evolving roles of commercial banks and the unique characteristics of digital money.

Traditional players, particularly commercial banks, will need to overcome challenges in adapting to this new tokenized finance paradigm. The first challenge is the capital investment required to explore potential projects. Then banks face a decision on whether to develop their business on private networks or create appropriate safeguards on public chains.

The former option gives banks greater control over who they transact with while the latter can provide the wide access necessary to scale solutions. Regulatory hesitancy, especially in the United States, can limit banks' experimentation with public blockchains. However, experiments in driving liquidity on private networks are still underway, and one could prove successful.

Another major challenge is the complexity of aligning on standards. To build interoperable networks, banks need shared standards for tokenization processes, accounts, tokens, identity verification, bridging, governance, and data privacy among other things. These standards are crucial for ensuring regulatory compliance and deriving the benefits of cross-protocol composability. Initiatives like Ethereum Improvement Proposals (EIPs) and Ethereum requests for comment (ERCs) offer standardized processes on the Ethereum blockchain that banks and market infrastructure firms have already begun to adapt. Standards also must be developed for interoperability between blockchain and legacy systems to ensure a smooth transition. As a way to align incentives for standardization, some consortia are exploring joint deposit constructs under which commercial banks would jointly issue a deposit token through a shared vehicle.

On the flip side, a significant enabler would be a regulatory environment that strongly favors existing institutions, coupled with the introduction of tokenized reserves or wholesale CBDCs (wCBDCs) exclusive to banks. This would continue to facilitate settlements between banks and potentially allow more coordination around integrating existing banking systems and these novel networks. With nearly 60% of central banks expecting to issue a wCBDC in the medium term, the collaboration between central banks and private sector entities will be critical for the evolution of the banking system. For instance, the Banque de France's experiments with the private sector have shown that wCBDC networks built with the private sector can enhance money's singleness, streamline trade processes, and bolster financial stability. Operationalizing these findings on a global scale would accelerate the adoption of blockchain-based financial infrastructure and help ensure a leading position for traditional financial institutions in the future of money.

Rise of Digital Intermediaries

Digital disruptors are beginning to gain market share by providing effective custody and trading solutions aimed at underserved segments. Today that includes firms in the crypto space, with exchanges serving as on- and off-ramps enabling investors to access the crypto ecosystem and disruptors providing services to web3 firms, but that expertise could expand to other markets.

These new intermediaries will likely scale their efforts via targeted use cases and collaborations. These collaborations may also include banks, as already observed in the tokenized treasury market today. Traditional institutions have also launched their own digital offshoots. The middle market of commercial banks that cannot invest in new technology directly may begin to partner with digital disruptors, especially as the disruptors move up and across markets. These types of collaborations provide disruptors with greater legitimacy and opportunities to expand into adjacent markets. Likewise, digital natives are well positioned to partner with DeFi players, providing regulated access to the innovation happening in public chains. In this partnership, digital natives help provide scale to DeFi protocols by specializing in regulation and institutional client needs.

Further institutional and policy development is needed to continue to build trust. Regulatory clarity, improved disclosure, anti-fraud protections, and suitability requirements are all necessary for the rise of digital intermediaries. Policymakers have been busy proposing stablecoin regulatory frameworks, with the Financial Stability Board having finalized a global regulatory framework for cryptoasset activities and global stablecoins in July 2023. However, regulators in many countries, including the United States, remain uncomfortable with permissionless networks. As the middleware layer between permissionless networks and real-world use cases, digital disrupters risk serious fines by leveraging public blockchains for their product offerings in these countries.

Success breeds success, and liquidity could gradually build as digital intermediaries facilitate access. Use cases will need to be sizable or scale with other uses cases and be seamless for clients to engage with. Over time, narrow money tokens can become treasury currencies. Some digital disruptors will focus on building e-wallet solutions, enhancing user interfaces, and facilitating integrations between systems. They will do this most effectively in jurisdictions with regulatory clarity, as they effectively wrap innovation on public chains into a traditional legal structure desired by non-crypto natives. These services will also appeal to other innovators open to experimentation, like other fintech players, who would likely be early adopters.

With sufficient momentum, policymakers may eventually support narrow payment tokens with some level of central bank support. Gaining access to central bank money — either through an omnibus account for real-time gross settlement or the discount window — would eliminate counterparty risk, thereby legitimizing these money tokens and further encouraging companies to adopt them for payments.

Universal Networks

Universal Networks represent a significant departure from the status quo in financial markets. Leveraging DeFi structures and business models, these networks aim to offer a peer-to-peer and highly automated alternative to the current system.

Access to Eurodollars in emerging markets may be the first high-value payments use case unlocked on public chains. The number of stablecoins and tokenized treasuries issued on public chains has been expanding. In emerging market economies that lack developed short-term borrowing markets, access to these tokens can offer exposure to dollarbacked instruments as well as financing opportunities. This will be attractive to firms that may be underserved currently.

If the DeFi model proves successful, public networks could attract additional flows and innovation. The creation of new products brings more assets on-chain, fostering an open marketplace. Innovative decentralized applications (dApps) for wholesale payments facilitate exchange across payment forms. These dApps leverage novel mechanisms such as automated market makers (AMMs) and automated liquidations on collateralized loans. Proven governance models and more sophisticated tokenomics fuel growth, and institutional investors gain comfort with this bottomup innovation. The result is more ways to participate and manage complexity at a lower cost. Open innovation also could lead to the development of new risk management solutions that could allow a broader range of investors to invest in these products.

Public chains will need to overcome significant challenges to reach scale and support information discoverability. Many public chains have historically prioritized decentralization and security over scalability, which has led to low transaction per second capacity and fee spikes during high traffic. And while off-chain data storage can increase throughput, that approach introduces concerns around data resiliency and centralization risks. Ensuring a balance between compliance and privacy will also be necessary. Privacy in public chains today can be breached because it is relatively straightforward to deanonymize wallet addresses, which drives some trading activity to over-the-counter desks. Various institutions are developing encrypted transactions (or encryption mechanisms for transactions), but concerns around privacy also will need to be balanced with compliance requirements. Leaving any of these challenges unresolved would create an opportunity for centralized solutions to emerge and move toward the rise of digital intermediaries vision.

A desire for interoperability may bring TradFi players on-chain who were previously experimenting on private networks. For example, banks could push for so-called Institutional defi solutions, which combine DeFi protocols with appropriate safeguards. An important enabler will be successful advances in digital identity solutions that provide a “trust layer” on top of DeFi. Trust credentials make private smart contracts on public chains viable and allow for regulated use cases to flourish on permissionless networks. Such a level playing field could lessen the advantages currently held by the largest and most well-connected firms. Fierce competition in an open network would likely favor specialization on specific products and services by different players, over time unbundling commercial bank offerings.

Yet this vision of universal networks confronts significant regulatory and technical challenges. The adoption of public chains would require a significant shift in regulatory frameworks, both within and across countries. Project Atlas is an ongoing attempt by the BIS and several European central banks to track and understand cross-border DeFi activity, which could be an early step toward understanding where it makes sense to apply regulation. Some countries, such as Singapore, are encouraging experimentation, even if restricted to institutional use cases. On the other hand, countries without regulatory guidance may fall victim to regulatory arbitrage, with innovation moving offshore. Most commentary from international organizations, including the BIS, is distinctly negative on public chains. On the other hand, the BIS has advocated for building a universal ledger, so it is possible that central banks might coordinate to set up a permissioned universal network.

Sovereign Expansion

The concept of Sovereign Expansion represents a significant shift in the role of central banks and the utilization of CBDCs.

The degree of flexibility that central banks have in shaping the future of tokenization and digital money depends on when they decide to engage. Jurisdictions that take an early, active role will have a greater ability to co-design with the market what shape tokenized networks take on locally, as well as the role tokenized reserves will play in the market. On the other hand, later jurisdictions will likely have to contend with existing market developments. While central banks will always enjoy wide latitude to enact policy, the full set of choices will eventually narrow. Central bank options may look quite different in a world leaning toward a bank-dominated paradigm than one in which significant activity has shifted onto public networks.

The growth and scale of central banks in the financial ecosystem could be driven either by slow changes over time or in response to a crisis that requires central bank intervention. Upgrades to RTGS and current wholesale payment solutions are already underway, and tokenized reserves could potentially replace these existing systems over the medium- to long-term. As more assets become tokenized, participants in high-value transactions may prefer to make use of tokenized central bank money as the safest on-chain solution. Such increasing demand from market participants could lead central banks to expand the types of institutions allowed to hold and transact in tokenized central bank money. Some countries, like Brazil, are already planning to do so.

Alternatively, investors and corporates may demand access to CBDCs for safety and efficiency in response to crises. Electronic money has already proven to exacerbate bank runs, and programmable money could accelerate them further. To the extent the financial system relies on fractional reserve banking, which we find unlikely to change at least in the short- to medium-term, this danger will exist. In the case of a major crisis like cascading bank runs, access to tokenized central bank money may expand rapidly as a means to backstop the system. Similarly, there could be a formalization of issuers that tokenize government securities. The end result would be the same as gradual change: tokenized central bank money comes to replace most money used today for high-value payments, and perhaps expands to everyday citizens in the form of a retail CBDC.

Such an outcome could expand central bank capabilities in an appealing way for policymakers, giving them additional control over the monetary system. While controversial, a programmable interest rate on money is an example of a new tool available to central banks. Political demand and public support for a change in the role of central bank money also could enable this expansion, perhaps in response to digital asset alternatives that begin to gain traction and challenge sovereign currencies like the dollar, euro, or yuan. We are already seeing how dollar-pegged stablecoins are challenging national currencies in emerging market economies around the world. If high inflation continues to plague advanced economies, we could see similar dynamics play out there as well.

As we enter a new phase of market competition driven by digital money and tokenization, the implications for industry players are consequential and interconnected. Whether you're a CFO, policymaker, bank strategist, or digital disruptor, understanding the broader landscape is crucial. We offer insights tailored to specific roles, but each contains a piece of the larger puzzle that is invaluable for anyone invested in the future of money.

For these public-sector officials, tokenization presents a double-edged sword. On one hand, it offers a compelling mechanism to deepen capital markets and fuel economic expansion. On the other hand, the proliferation of tokenized money could challenge the unified nature of currency and necessitate adjustments in monetary policy. The tokenization of government securities, coupled with evolving regulatory landscapes, will be instrumental in shaping the future of money. Whether as collateral for stablecoins or directly fractionalized and used as a medium of exchange, government bonds will play a far more direct role in money creation. Additionally, governments must consider how to respond in the event of a financial crisis, which could force them to assume a far more significant role in financial markets.

Banks face existential questions as tokenization and new forms of money challenge their traditional business models and custodianship of customer assets. The possibility of self-custody and capital markets expansion raises the question of how to protect revenue if banks lose client relationships and deposits. The survival and competitiveness of banks may hinge on early investments, strategic partnerships, and their ability to leverage commercial networks to develop compelling offerings. Banks that are proactive will influence future industry standards and ensure their relevance in an evolving financial ecosystem, but they will need to remain alert to the risk that DLT-inspired technologies trigger the unbundling of banking services in the high-value space.

Asset managers face both significant opportunities to expand their offerings and a meaningful risk of disruption in a world that increasingly relies on technology to manage money. With new tools at their disposal, asset managers can leverage their expertise in money market funds to issue yield-bearing stablecoins that compete with bank money. They also have an opportunity to facilitate credit creation in capital markets by designing and selling shares in novel funds that extend credit to hedge funds and corporations. If the ecosystem builds new KYC and AML tools, it could be easier to manage funds across geographies. At the same time, as more finance moves on-chain, the ability of asset managers to discover and interpret real-time information will be critical. Tech-savvy challengers may exploit their advantage in this area to replace the asset managers of today as the barriers to competition come down. Asset managers will be compelled to make substantial investments in cultivating new capabilities.

Digital intermediaries stand poised to revolutionize finance by leveraging tokenized assets and money to deliver superior financial products for corporates and asset managers. Their success hinges on mastering cross-network custody, compliance, and connectivity, enabling them to simplify the user experience by masking technological complexities. This could be unlocked through collaborations with industry platforms such as treasury and merchant solution providers. Specialized money issuers will need to emerge for disruptors to challenge banks at the core of their business model: deposits and payments. A major factor in this competition will be regulation, with access to central bank reserves a defining goal for any privately issued narrow money.

Fully peer-to-peer financial networks, as observed in the crypto space, are the culmination of an increasingly techmediated financial system, but it is far from assured they will gain institutional scale. Open platforms allow for the effortless deployment and customization of financial products and services, driving innovation and specialization. Crypto natives have an edge in expertise and nimbleness to innovate. Their challenge will be to overcome technical barriers that prevent interoperability and scalability while also delivering compliant solutions. Builders must establish a trust layer over DeFi to successfully meet regulatory challenges, and even then, existing laws will need significant revisions to fully accommodate this future. If they can succeed, digitally native yield-bearing assets and innovative risk-distribution protocols would become the foundation of a radically new financial system.

Digital money and tokenization are innovations that offer novel avenues to balance liquidity with yield, which will unlock new strategies for liquidity management and working capital efficiencies. Programmability and atomic settlement will help reduce counterparty risk and increase the speed of financial flows. At the same time, these advances also introduce new types of technological and operational risks, requiring a reevaluation of existing risk models. As the financial ecosystem evolves, CFOs may need to contemplate whether their long-standing banking partners can keep pace with innovation, or if alternative advisors may better serve their objectives.