Decentralized finance (DeFi), which uses blockchain-based smart contracts to execute a variety of financial services activities, has seized the attention of technology developers, investors, and financial institutions. DeFi protocols have already enabled nascent markets in the crypto-asset industry on public blockchains, such as borrowing and lending as well as decentralized exchanges. Imagine the potential if the technology were to be applied to streamline transactions in foreign exchange, equities, bonds, and other real-world assets. This will require the creation of digital representations, or tokens, of real-world assets to bring them onto the blockchain. The cost savings and new business opportunities of creating a “tokenized” version of real-world assets for transacting through DeFi protocols could be significant for issuers and investors, as well as for financial institutions that can adapt their technology and business models.

That’s an alluring prospect, but many DeFi protocols today are not designed for use in mainstream finance. Firms that wish to apply DeFi in their client offerings must incorporate the same, if not higher, levels of safeguards and security standards that have been developed over decades in the finance industry.

Financial services are built on trust and empowered by information. This trust rests on financial intermediaries who maintain the integrity of records covering ownership, liabilities, conditions, and covenants, among other areas, across a variety of siloed ledgers that are separate from the means they use to communicate. As each intermediary has a different piece of the puzzle, the system requires much post-transaction coordination to reconcile the various ledgers and settle transactions. For example, many securities transactions, particularly cross-border ones, can take anywhere from one to four days to settle.

Distributed ledger technology (DLT), such as blockchain, has the potential to resolve some of those inefficiencies by presenting transactional and ownership information on a single shared ledger. The growing acceptance of tokenization, which creates digital representations of assets such as a stocks and bonds on a blockchain, can extend the benefits of DLT to enable exchange and settlement of a wide range of asset classes. Institutions can generate further efficiency by adopting DeFi protocols, which use software code to automatically execute a range of financial transactions pursuant to preset rules and conditions.

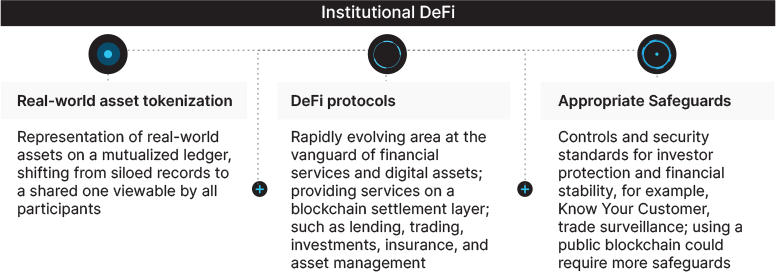

We define Institutional DeFi as the application of DeFi protocols to tokenized real-world assets, combined with appropriate safeguards to ensure financial integrity, regulatory compliance, and customer protection. (It is important to note that in this joint paper we do not refer to Institutional DeFi as institutional players participating in crypto DeFi.) The prize for innovators who hone this model for use in the world’s trillion-dollar finance industry could be substantial.

Exhibit 1: What Is Institutional DeFi?

Source: Oliver Wyman Forum, DBS, Onyx by J.P. Morgan, SBI Digital Asset Holdings

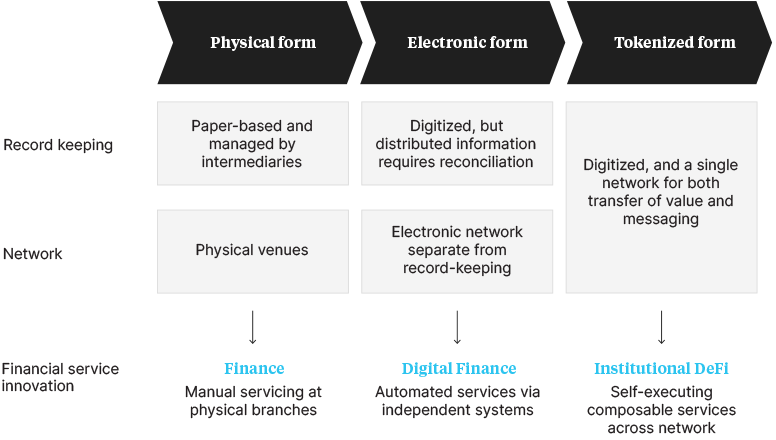

Technology continually evolves and modernizes financial services by creating new ways of executing and recording transactions. Each step in this evolution brings new business opportunities. For example, dematerialization replaced paper certificates with digital ones in the form of electronic book-entries, fostering the rise of electronic payments and trading. That, in turn, made securitization possible, which added value to previously illiquid assets such as mortgages.

Despite recent waves of digitization, trillions of dollars’ worth of real-world assets are recorded in a multiplicity of ledgers that remain separate from messaging networks. This means that financial intermediaries have to record transactions on siloed ledgers and then message each other to reconcile their books and finalize settlement. The need for coordination across ledgers and networks between entities creates inefficiencies that increase costs and risks, lengthen settlement times, and in general add overhead to financial services.

The past few years have witnessed an increased focus on blockchain technology as a potential panacea for resolving these inefficiencies. The promised value of blockchain comes from combining ledgers and networks in a way that allows multiple parties to see the same information, hence greatly reducing the need for reconciliation after a trade or transaction. In addition to creating a shared view of information (transaction balances, ownerships, etc.), blockchains also enable business rules and logic to be executed and viewed with high transparency and in a deterministic manner. For example, lending business logic can be codified transparently in smart contracts, thereby enforcing adherence to rules and automating settlement.

Exhibit 2: History of Asset and Money Representation

Source: Oliver Wyman Forum, DBS, Onyx by J.P. Morgan, SBI Digital Asset Holdings

In the process of adopting blockchain technology, financial firms are exploring representing real-world assets as tokens on a blockchain. Such tokenization can reduce settlement risk and decrease settlement times, which typically takes one to two days even for low-risk assets such as G10 government bonds, by enabling so-called “atomic” settlement – the instant exchange of two assets on the condition that assets are simultaneously transferred. No party to a transaction is then left waiting for delivery.

The application of smart contracts in asset tokenization also has delivered a number of benefits, including enhanced and new offerings. For example, J.P. Morgan leverages tokenization to offer intra-day repo solutions for clients on its Onyx Digital Assets platform, and DBS Digital Exchange offers corporates a platform to raise capital through the digitization of their securities and assets, with options to offer smaller denominations.

These tokenization benefits are also welcomed by asset managers, as 70% of institutional investors expressed willingness to pay extra for increased liquidity and faster asset turnover, according to a recent survey conducted by Celent.

Tokenization efforts in the industry are well under way covering both payment instruments and assets, which creates the potential for end-to-end asset exchange on blockchain.

In parallel to industry efforts to develop real-world asset tokenization, the concept of decentralized finance has flowered in the public crypto-asset space. DeFi, as it is popularly known, refers to decentralized applications (DApps), which provide financial services via sophisticated and automated computer code on a blockchain as the settlement layer. These services include payments, lending, trading, investments, insurance, and asset management. DeFi protocols are the code and procedures that govern these applications. These protocols typically operate without centralized intermediaries or institutions, use open-source code, and allow for flexible composability (code or applications can be taken from one protocol/service and plugged into another).

DeFi has rapidly emerged in the past three years and grew more than tenfold to $160 billion in 2021 in terms of total value locked before retreating to stand at a little over $50 billion as of October 2022. DeFi innovations have flourished across various financial ecosystems and attracted billions of dollars of liquidity across decentralized exchanges (such as Curve and Uniswap), lending protocols (such as Aave and Compound), and other DeFi solutions, such as liquidity staking and collateralized debt positions, which lock up collateral in a smart contract in exchange for stablecoins.

Some noteworthy innovations in the DeFi space involve crypto lending/borrowing protocols and decentralized exchanges:

DeFi, as described above, is prevalent in the public blockchain space and applies mostly to transactions in the largely unregulated crypto-asset industry. Yet the logic embedded in DeFi protocols, which are programmable, self-executing business processes, can be applied to interact with any tokenized asset.

Building full-scale financial services that leverage tokenization and programmability could have far-reaching implications for the finance industry. It could generate substantial cost savings, as code dramatically reduces middle- and back-office operations across firms and intermediaries. In the exhibit below we list some notable benefits of DeFi solutions. New business opportunities are also likely to emerge as financial institutions take advantage of the composability of DeFi protocols, packaging multiple DeFi protocols together to offer new solutions. First, however, firms must adapt the DeFi protocols to the regulatory standards of today’s trillion-dollar markets for money, stocks, bonds, and other assets.

Today’s finance industry rests on an array of safeguards that protect investors from fraud and abusive practices, combat financial crime and cyber malfeasance, maintain investor privacy, ensure that industry participants meet certain minimum standards, and provide a mechanism for recourse in case things go wrong. Institutional DeFi will need to incorporate the same, if not higher, level of standards to meet regulatory requirements, create trust, and drive adoption by issuers, investors, and financial institutions.

Here are some of the key safeguards needed to build DeFi-based solutions for institutions:

While Institutional DeFi has potential, financial institutions need to consider areas where tokenization and programmability are most valuable, and tailor DeFi protocols for their purposes accordingly instead of simply reusing what works in the crypto-asset industry.

Institutions interested in exploring Institutional DeFi solutions should start by asking themselves, “why DeFi?” The answer will depend on the commercial viability, adoption feasibility, and competitive advantage of such a solution. Objectives could range from creating new products and reducing data reconciliation tasks, to cutting costs and speeding up settlement times.

Firms also need to consider a number of broader objectives when designing Institutional DeFi solutions. These should include:

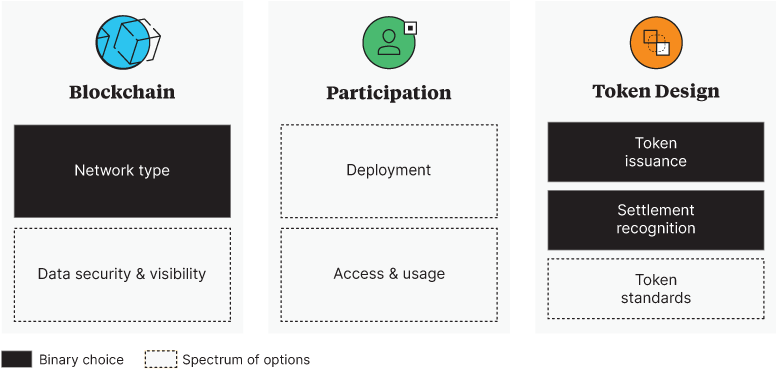

After firms have established their objectives, they need to make choices in three key areas: Blockchain, Participation and Token Design. It is critical that firms weigh the options and their associated trade-offs carefully, as these design choices are paramount in influencing how the offerings achieve their objectives.

Exhibit 4: The Three Key Design Choices

Source: Oliver Wyman Forum, DBS, Onyx by J.P. Morgan, SBI Digital Asset Holdings

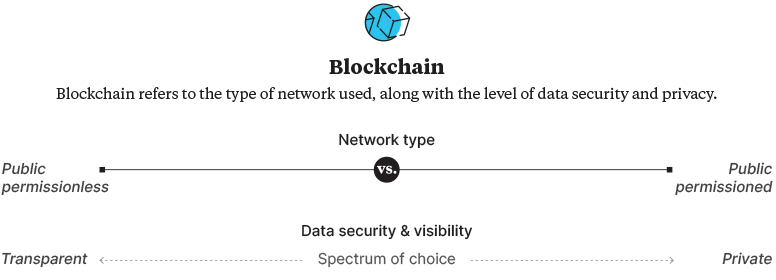

Exhibit 5: The Three Key Design Choices - Blockchain

Source: Oliver Wyman Forum, DBS, Onyx by J.P. Morgan, SBI Digital Asset Holdings

- Network type – Network type refers to the underlying network and database used to deploy an Institutional DeFi solution with asset tokens. This design choice is critical because it affects so many important design objectives, such as user access, interoperability, and the strength of the developer ecosystem.

Read More

Public permissionless networks, such as Ethereum and Polygon, impose no restriction on access, and therefore have the potential to encourage wider participation. They are better equipped to facilitate interoperability with existing digital assets and DeFi protocols, which are on public permissionless networks. There is already a wide base of DeFi developers and open-source code that have been tested and deployed on public permissionless networks. This helps kickstart and facilitate continued innovation, using software components and applications that are leverageable and composable. On the flipside, this openness is also a potential source of risk unless additional safeguards are put in place.

Public permissioned networks, on the other hand, can facilitate the use of controls to authorize user access and restrict the visibility of transactions on these networks. This enables easier implementation of checks and balances, along with traceability for investigation purposes. As Institutional DeFi models are still being explored, it is possible a public permissionless blockchain could be modified to ensure it is usable at scale by institutional participants.

- Data security and visibility – This informs the level of data transparency of the solution, and its implied level of data security.

Read More

Data transparency is itself a multifaceted concept and the choices vary along a spectrum. On one end of the spectrum, all transaction data is transparent and available for all participants to view, as is common with many public blockchains today. On the other end of the spectrum, participants may access only data relating to their own transactions. Function-level access management can provide different levels of access to users, while encrypting data and providing a viewing key to selected participants can enable authorized viewership. Moreover, different techniques, such as zero-knowledge proofs (ZKP) and ensuring DeFi protocol uses only private messages, can be implemented for data privacy on public blockchains.

The choice of transparency level primarily depends on the solution’s value proposition – but data ideally should be private while discoverable to customers or authorized stakeholders (such as regulators). For example, the preferred approach for a central limit order book-based venue may be to make order and transaction data available, while a dark pool solution may prefer to conceal order information.

Mechanisms for data management and protection need to be properly designed to comply with regulatory data requirements to prevent issues introduced by DeFi such as maximal extractable value (MEV), where each of the validators or “miners” updating the blockchain can determine which transactions are executed and when, thus affecting market prices and opening the door to front-running and other forms of market manipulation. This is especially important for solutions on the public blockchain as data is permanently and immutability recorded on a publicly available ledger, introducing a higher risk of loss of privacy.

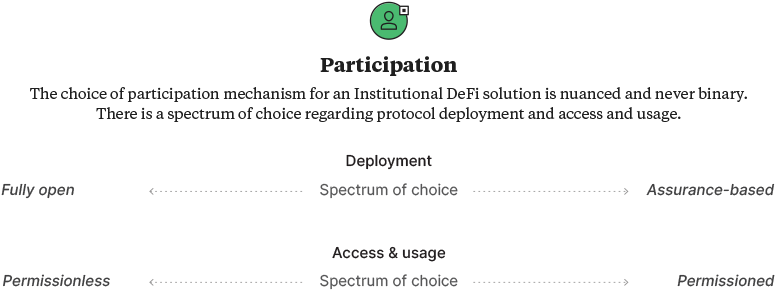

Exhibit 6: The Three Key Design Choices - Participation

Source: Oliver Wyman Forum, DBS, Onyx by J.P. Morgan, SBI Digital Asset Holdings

- Deployment – This choice governs how new smart contracts and protocols are developed and deployed, and embodies different approaches to innovation and risk.

Read More

On one end of the spectrum, in a fully open model, anyone can develop and deploy smart contracts. This lowers barriers for application development and encourages competition, but it also entails risk as there are fewer checks and balances before protocols are deployed. This is not to say that assurance standards are not used. For example, some DeFi protocols today make use of code audits. But such standards are not mandated nor instituted for deployment. On the other end of the spectrum, in an assurance-based model, control and review/approval mechanisms are put in place to ensure adherence to specific standards before deployment. These can be industry standards widely accepted by institutional investors and clients or standards instituted through regulatory requirements. One approach is to allow only selected developers or firms to develop new processes. Another approach is to ensure specific checks are made to protocols, allowing only verified protocols to be deployed.

- Access and usage – This design choice relates to how controls are put in place to manage user access and usage.

Read More

Restrictions can be imposed at the service level (such as by controlling who can access a liquidity pool) or at the level of underlying functions (for example, by controlling trading permissions, such as instrument types and ticket size). A permissionless participation model is one where anyone can access the DeFi protocols and use all functions without restrictions (such as the Uniswap DEX), while a permissioned participation model is one where only authorized or verified participants can access specific services and use selected functions. While a permissionless participation model could help maximize the potential userbase and foster growth, a permissioned participation model helps comply with regulatory requirements (such as KYC, qualified access) by ensuring only the right participants can use the appropriate functions. Note that a permissioned model can still be enabled on a public permissionless blockchain, via access management mechanisms.

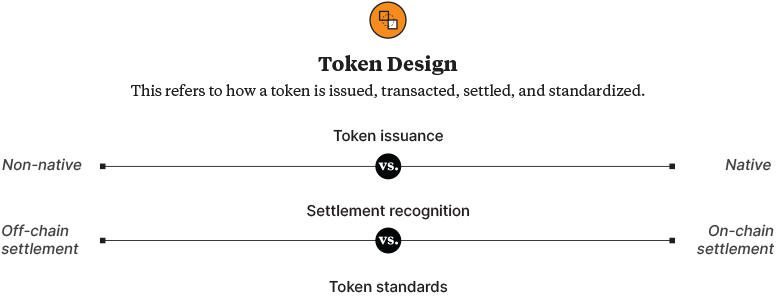

Exhibit 7: The Three Key Design Choices - Token Design

Source: Oliver Wyman Forum, DBS, Onyx by J.P. Morgan, SBI Digital Asset Holdings

- Token issuance – Non-native tokens are issued to represent existing real-world assets.

Read More

These non-native tokens are bound to existing off-chain processes and control mechanisms, such as custody and reconciliation. For example, on the Onyx Digital Assets platform, securities accounts holding US Treasuries maintained by J.P. Morgan for the benefit of its clients are tokenized to enable intraday repo transactions. On the other hand, real world assets can be issued directly on a blockchain as native tokens, such as through security token offerings (STO). It is worth noting that asset tokenization is rapidly evolving, and there may be more ways to issue tokens in the future.

There is currently legal uncertainty involved for both native and non-native tokens. Depending on the nature of the native token’s asset class, there can be a lack of legal clarity on whether such native tokens can exist by themselves and rely on the blockchain alone for record of its existence. For example, bonds in the EU have to be registered with a central securities depository (CSD), and having a natively issued bond token without separately registering with the CSD may not meet such requirement. We note that this leaves space for innovation in regulation as well as the creation of blockchain-native CSDs and similar actors. For non-native tokens, there are considerations such as on-chain settlement finality, which we discuss in the next sub-section.

Both non-native tokens and native tokens can interact with DeFi protocols, allowing for automatic execution of asset servicing and transactions without the need to rely on legacy systems. However, transactions with non-native tokens may ultimately require interactions with off-chain processes as noted above. The choice of token issuance will depend on the nature of the asset which is intended to be reflected, whether such asset requires linkage to an off-chain asset, whether blockchain ledgers may serve as the determinative books and records in respect of the issuance and ownership of such asset, and whether there is the desire or need to tokenize an existing asset that lives in legacy off-chain systems.

- Settlement recognition – Settlement recognition depends on whether or not a token transfer on-chain is recognized by law, regulation, or contractual arrangement as a final transfer.

Read More

This is a notable issue for consideration in respect of non-native tokens, where additional steps may be required to be taken with respect to the off-chain asset being represented. However, as noted above in respect of CSD registration requirements, this issue may arise due to regulation in respect of native tokens as well. Off-chain settlement is when a token transfer is not recognized as a transfer of the underlying asset. In this case, settlement finality is recognized off-chain, in which an off-chain ledger is updated to reflect ownership change. On-chain settlement is when settlement finality is recognized on-chain, whereby the on-chain ledger is recognized as the single source of truth for transfer and ownership.

The determination as to whether settlement can be recognized on-chain mainly depends on whether regulators and transaction participants can legally recognize the blockchain records as the final books and records of transactions, allowing the blockchain to function also as a de facto ownership ledger. This requires an understanding of the regulation and commercial law applicable to the transaction at issue, as well as any contractual arrangements in place. The analysis here will determine whether transactions need to rely on legacy ledgers and processes, or whether legacy systems can be entirely replaced.

- Token standards – Token standards are the set of principles on which tokens are issued and smart contracts are developed.

Read More

These standards influence the ability to interact with different DeFi protocols, and hence the interoperability and functionality, of the asset tokens. Different public standards might be appropriate depending on the type of token to be issued. For example, the ERC-721 standard is designed for non-fungible tokens (NFTs) while ERC1155 is suitable for both fungible and non-fungible tokens and can be explored for tokenized assets.

Experimentation is crucial to understanding different approaches to Institutional DeFi. Finance industry participants around the world are increasingly conducting pilots and experiments to explore different design objectives and choices.

This report draws on the hands-on experience of the co-authors in running a joint pilot under Singapore’s Project Guardian. The Monetary Authority of Singapore (MAS) launched this collaborative initiative with the financial services industry to explore the economic potential and value-adding use cases of asset tokenization and DeFi. Using a controlled, sandbox environment, it aims to test the feasibility of applying asset tokenization and DeFi protocols, while managing financial stability and integrity.

Project Guardian is designed to help MAS build a digital asset ecosystem framework, develop and enhance relevant policies, and provide direction on technology standards. Project Guardian will test the feasibility of applications in asset tokenization and DeFi, while managing risks to financial stability and integrity. The central bank aims to develop and pilot use cases in four main areas:

Exhibit 8: Project Guardian Objectives

Source: Oliver Wyman Forum, DBS, Onyx by J.P. Morgan, SBI Digital Asset Holdings

In the first pilot, our co-authors gained first-hand experience in implementing DeFi solutions in the financial markets, including foreign exchange and government bond markets. This section details the pilot’s business objectives, design choices, and the lessons learned to date.

Pilot One was led by co-authors DBS, Onyx by J.P. Morgan, and SBI Digital Asset Holdings. It sought to determine whether tokenized real-world assets and deposits could be transacted on a public blockchain leveraging DeFi protocols, in a compliant manner that preserves financial stability and integrity. The intent was to explore the delivery of traditional financial services in a more open manner, fostering broader participation in foreign exchange and government bond markets through an open and efficient ecosystem that attracts liquidity providers and liquidity takers.

There were two workstreams in this pilot to ensure comprehensiveness. Workstream one focused on foreign exchange transactions using SGD tokenized deposits issued by J.P. Morgan and JPY tokenized assets issued by SBI Digital Asset Holdings, and workstream two focused on the trading of foreign exchange and government bonds using tokenized cash (deposit) and tokenized securities between entities of DBS and SBI Digital Asset Holdings. Transactions under both workstreams were conducted on public blockchain main net, focused on technical and operational feasibility, and participants established bilateral terms and other controls to avoid actual financial impacts, such as planned trade unwinding for workstream one.

To fully assess the efforts needed for the implementation of Institutional DeFi, the pilot went through the complete lifecycle from trade order placement to trade execution, token settlement and clearing. Relevant business and operational teams from front office to back office were involved to assess potential gaps ahead of the potentially scaled implementation of Institutional DeFi, reducing adoption friction and encouraging internal buy-in.

Transactions were executed using modified public DeFi protocols and leveraged Verifiable Credentials issued by trust anchors to ensure transactions were executed in a safe and compliant manner.

We illustrate the design choices made under the four focus areas:

Exhibit 9: Guardian Pilot Setup

Source: Oliver Wyman Forum, DBS, Onyx by J.P. Morgan, SBI Digital Asset Holdings

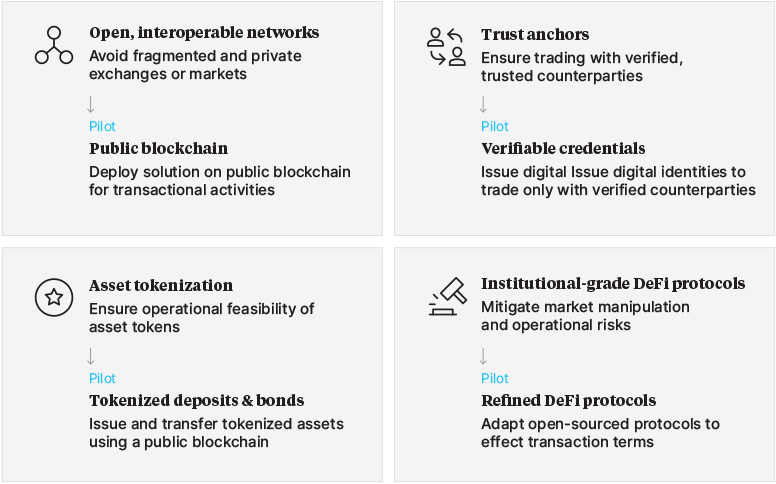

- A public blockchain, Polygon was selected for its potential to allow higher interoperability of tokenized real-world assets and DeFi protocols, which allowed participants to develop their own solutions based on a set of agreed upon technical standards.

- Trust anchors were developed to ensure all trades were conducted within a controlled, trusted environment. W3C Verifiable Credentials issued by trusted financial institutions were used to enable compliant access to the DeFi protocols. Verifiable Credentials consisted of tamper-resistant information (identifiers and metadata) that cryptographically attested to the identity of the entity/person using them. These credentials were developed using W3C standards to reinforce Project Guardian’s interoperability objective.

- The pilot leveraged tokenized assets created by the co-authors across two workstreams. In workstream one, Onyx by J.P. Morgan focused on tokenized Singapore dollar (SGD) deposits and SBI Digital Asset Holdings focused on tokenized Japanese Yen (JPY) assets. In workstream two, DBS focused on tokenized SGD deposits and tokenized Singapore Government Securities (SGS), and SBI Digital Asset Holdings focused on tokenized JPY deposits and tokenized Japanese Government Bonds (JGB). Our co-authors played unique roles to complete bilateral trades within these work streams.

- Participants used modified public DeFi protocolsto conduct the transactions – a lending and borrowing protocol (Aave) was applied to a foreign exchange use case in workstream one, and a decentralized exchange protocol (Uniswap) was applied to the trading of foreign exchange and government bonds.

The pilot found that DeFi protocols have potential to be adapted and tailored for foreign exchange and government bond markets activities on a public blockchain. Further details of the pilot will be explored in subsequent sub-sections. Continuous improvements and testing of solutions are on the horizon to better serve participants’ circumstances, needs and objectives. The use of specific protocols by the pilot participants does not constitute an endorsement of such protocols by any author of this report. The participants will continue to experiment, both adapting existing protocols and building new ones. Independent judgment should be exercised in selecting an appropriate protocol to suit any individual’s or organization’s circumstance, needs, or objectives.

Among multiple design aspects, our coauthors believe at least two were critical:

- A trusted compliant method – Trust anchors and Verifiable Credentials were used to authenticate identity and connect with existing legal frameworks. Trust anchors were regulated financial institutions that verified and issued Verifiable Credentials to participating traders, enabling them to transact on the public blockchain. The trust anchors can be viewed as the universal trust layer, providing participants with a compliant gateway to the Institutional DeFi solution.

The implementation of the trust anchor mechanism was flexible and could vary across institutions. For example, authorized traders were issued credentials by their parent institutions, through various internal processes and credential issuing software. These credentials were attached to trade instructions to the DeFi pool, and on-chain verification of these credentials ensured that only instructions with legitimate credentials were forwarded to the DeFi pool. - Alignment on technical standards – Standards such as ERC-20 and W3C were used to allow potential interoperability among pilot participants.

The participants aligned on technical standards to allow interoperability between specific DeFi protocols and existing legacy off-chain systems. Interoperability also drove the choice towards the use of ERC-20, the most common token standard in the Ethereum ecosystem, to define token ownership, supply, type of issuance, and data to be stored on-chain, such as the token name and ticker. Moving forward, there may be other standards such as ERC-1155 that could better represent traditional instruments on-chain and for trading. The Verifiable Credentials were developed based on W3C standards to enable participants to transact in a compliant manner on a modified version of the permissioned Aave protocol on the Polygon network.

Exhibit 10: Summary of Project Guardian Design Choices

Scaling the solution to benefit global financial markets will require more work. From experience with Pilot One to date, our co-authors have jointly identified seven areas that would need broader industry efforts to build the scalable foundation for Institutional DeFi offerings.

#1 Legal clarity on frameworks

Participants need to actively identify areas that need clarity within the prevailing legal and regulatory framework and engage with regulators and legislatures to drive regulatory and legislative solutions that account for this new financial environment enabled by the new technology. These efforts should address issues such as recourse mechanism, on-chain settlement treatment, KYC and AML, usage and holding of crypto-assets, and legal and accounting treatment of business activities:

- Recourse mechanism – Existing legal recourse and dispute management processes may be insufficient to address potential disputes in a blockchain environment in the absence of separate contractual arrangement, especially for issues currently handled by an intermediary or agent. For example, crypto bridge Nomad alerted law enforcement about a loss from a cyberattack, but there was limited recourse as authorities could not retrieve the funds, and Nomad had to bear a $200 million loss. Pilot One utilizes bilateral agreements to resolve potential legal disputes and address this issue. A multilateral framework and pre-defined participation rulebooks could reduce legal complexity among more participants.

- On-chain settlement treatment – Token-based trading and settlement require enhanced forms of record keeping and synchronization across on- and off-chain ledgers. For example, transactions were recorded (manually) in Pilot One on an off-chain legacy system for reporting and auditing purposes. Clear guidelines are needed to clarify roles of on-chain and off-chain operations, such as accounting and redemption processes, to comply with regulations and controls.

- KYC and AML – Further regulatory guidance is needed with regards to dealings with KYC, AML, and sanction issues for on-chain financial transactions, given the pseudonymous nature of existing DeFi protocols. Pilot One’s Verifiable Credentials-based identity solution serves as an example of how to ensure each counterparty is a permissioned and trusted entity. The pilot established that trust mechanisms can be universally accepted despite being implemented in different ways as long as they adhere to a common fundamental standard.

- Usage and holding of crypto-assets – Different regulators have imposed different restrictions on financial institutions with regards to holding crypto-assets, which are needed to pay for verification/processing of the transactions (gas fees) on public blockchain networks. Regulation will play a key role in reducing this friction.

- Legal and accounting treatment of business activities – It is currently uncertain how to classify certain transactions that use DeFi protocols when there is an interaction with a common asset pool. For example, it is currently ambiguous, from accounting and legal perspectives, when and how to classify contributions into liquidity pools, as the transaction may be treated as a sale, an investment in a fund, or not recognized until a trader trades the asset against the pool. While Pilot One mitigated this ambiguity via bilateral agreements, clarity on accounting and legal recognition will be required at a broader level to achieve scale.

#2 Adoption incentives

In addition to the efficiency gains of Institutional DeFi solutions, appropriate incentive mechanisms could encourage scalable adoption. Novel tokenomics arrangements in the crypto-asset industry, which enable liquidity providers and developers to earn tokens as participation rewards, might not apply readily in mainstream finance. Targeted incentives will be needed to encourage adoption and such incentives are likely to differ across various stakeholders and participants. Further iteration is required as the Institutional DeFi space is at a very early stage of development.

#3 Guardrails or tools

To ensure transactions happen in a safe and trusted manner, preserve transaction privacy, and provide security assurance against potential hacks, more tools are needed to streamline DeFi protocol development and improve the integration experience to drive usage.

Pilot One participants engaged with third-party auditing services to conduct complete smart contract audits prior to deployment. Participants also used Verifiable Credentials to establish a strong framework for instituting trusted identities and the accompanying qualifications to “permission” the participation in the DeFi liquidity pools. Nonetheless, more can be done to facilitate industry adoption, such as establishing an industry-recognized smart contract standard for interoperability.

Other feasible actions include formalizing how Verifiable Credentials and similar solutions can be leveraged, limiting a trader’s access to company funds/assets, protecting against concepts such as maximal extractable value (MEV), and lowering the threshold for developers to deploy and participants to use Institutional DeFi solutions.

#4 End-to-end co-ordination

Orchestration between legacy systems and blockchain-based assets and business logic is required to enable process and data interoperability. Participants need to explore Institutional DeFi in a comprehensive manner, involving all relevant business lines and evaluating and updating existing processes to capture/realize the potential benefits. For example, as transaction data is recorded on a mutualized public ledger, workflows can be adapted to refer to the ledger instead of legacy systems for faster reconciliation. At a broad level, programmable smart contracts could enable a high degree of automation, transparency, and efficiency in financial transactions.

#5 Continuous test-and-learn and improvements

Modifying DeFi protocols to force-fit them for institutional use is a test-and-learn process. DeFi protocols are designed to ensure that key market metrics, such as interest rates, collateral haircuts, and the like, follow supply and demand dynamics of the assets trading within them. For Pilot One, some of these codified rules had to be tailored to force-fit the business objective, such as altering interest rates of the lending protocol to zero, to avoid unintended behavior during transactions.

#6 Alignment on industry-wide technical standards

Standardized, well-adopted frameworks lay a strong interoperability foundation on which DeFi applications could be built and interact. Furthermore, seeking and collaborating with like-minded participants – and moving from proofs of concept to production – are critical in creating such a foundation. The value of this approach was demonstrated by Pilot One’s rapid solution development by leveraging an Ethereum-compatible public blockchain, ERC token standards with W3C Verifiable Credentials standards, and open-source DeFi protocols.

#7 Refined business models

The pilot demonstrated that DeFi protocols can unlock benefits associated with tokenized asset transactions. A key value-add of using DeFi protocols is the ability to codify core and non-core functions within financial services. The use of blockchain as the book of records allows for potential minimization of post-trade reconciliations between participants, thereby reducing operational overhead. Other potential benefits include greater transaction transparency, lower settlement risk, as well as enhanced efficiency and trading velocity due to atomic settlement. Nonetheless, the use of DeFi could lead to alteration of existing business operations, requiring participants to refine business and operational models to capture the incremental business value.

We are seeing emerging efforts to tap into the value of Institutional DeFi and transform the finance industry by creating new solutions or enhancing existing ones. This process is still in its early days and more work is needed by both individual firms and the broader industry to scale these efforts.

In Sections 2 and 3, we showed how an Institutional DeFi solution can be designed to fit business objectives while navigating industry constraints. But we observed that more could be done at an industry level to lower the threshold for adoption and amplify the value to be unlocked.

Drawing on lessons learned from industry pilots, we see three areas where industry could work together (see exhibit 11). Coordination is essential for widespread adoption of Institutional DeFi. Siloed efforts create the risk of inconsistencies across the industry, potentially stymieing progress and porting existing challenges to this new technology; joint efforts maximize network effects via interoperability and are likely to accelerate adoption.

Industry participants will play different roles toward these ends. We will share perspectives of a general industry framework for roles and responsibilities but be mindful that each business and jurisdiction may require refinement based on its localized specificities.

Exhibit 11: Key Areas of Instituitional DeFi Adoption Efforts

Source: Oliver Wyman Forum, DBS, Onyx by J.P. Morgan, SBI Digital Asset Holdings

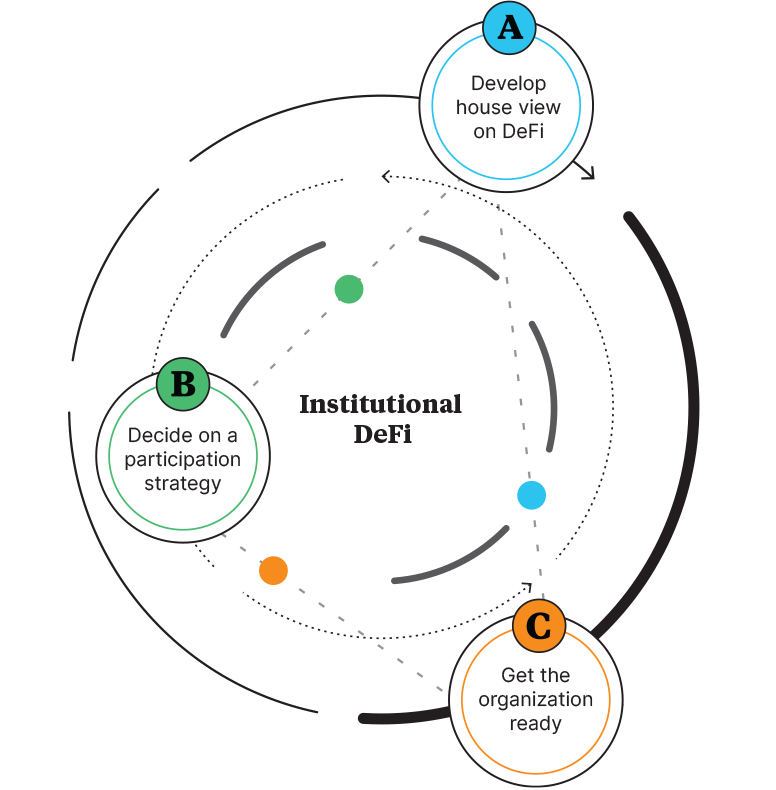

The rapid evolution of blockchain technology and the potential disruption it can bring requires institutions to get ahead of the curve to avoid being left behind. This is not meant to suggest every institution needs to be a leader, but it does require institutions to form a house view on the future of DeFi and the implications for the business, and then define the relevant participation and operating models to fulfill their ambitions. This is not a one-off exercise. It should be iterative given the dynamic nature of blockchain and DeFi protocols.

Exhibit 13: Key Actions to Build Playbook

Source: Oliver Wyman Forum, DBS, Onyx by J.P. Morgan, SBI Digital Asset Holdings

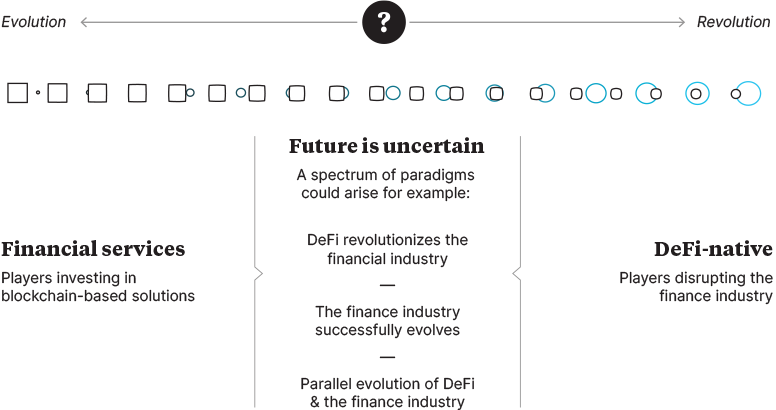

Institutional DeFi efforts are already happening and starting to bring change to the finance industry. The road ahead remains unclear, and the degree of change is likely to vary by business and market segment.

We see a spectrum of potential paradigms for the future of financial services, ranging from a modest evolution of existing market structures to a complete revolution that leaves DeFi triumphant. We already observe how both ends of the spectrum are driving change, with financial institutions starting to evolve and develop Institutional DeFi solutions while native DeFi players are looking to disrupt financial services with their decentralized solutions.

Exhibit 14: Potential Future Paradigms of Financial Services

Source: Oliver Wyman Forum, DBS, Onyx by J.P. Morgan, SBI Digital Asset Holdings

Change will likely be significant regardless of the paradigm that dominates, but the specific outcome will likely vary by market, jurisdiction, and business line depending on customer and regulatory acceptance. With all this uncertainty, it is important that industry participants take a scenario-based approach that enables them to examine multiple different potential futures while maintaining analytical discipline by requiring each scenario to use coherent and integrated assumptions. Based on these scenarios, firms could form a house view of the future and assess its implications for their business portfolios, profitability, funding costs, and the like. To get to that view, firms could consider three broad questions:

- What are the future scenarios shaping the industry and key watch points or triggers?

- What are the implications for our clients and competitors?

- What does this mean for our portfolio and financials?

Once they form their view of the future, firms could perform an impact analysis to assess the specific implications on their current business and financials while agreeing on the key watch points to monitor to potentially accelerate or pivot their responses. Depending on the scenarios used, regulatory developments, and the firm’s current position, implications could take on varying degrees of scale and urgency. Scenario analyses should aid senior management to align on a view of the future and implications for the business. Based on this, firms can then determine if, where, and how to participate, which we discuss next.

Exhibit 15: The Implications for Key Industry Sectors

Where should a firm play in the Institutional DeFi space? This is a question firms will need to work through in defining their strategy. In doing this, firms should look not only to transform existing end-to-end processes with new technology but also think about creating new businesses and new business models. According to a 2022 Celent survey of global institutional investors, 72% showed a preference for working with an integrated provider for all digital asset needs, indicating the need for significant upgrades to current investment management systems.

As strategy is all about trade-offs, being clear on the right trade-offs is critical to aligning an institution and putting in place guardrails to ensure that where and how it participates is in line with its risk appetite and other internal considerations. To think through this, firms may want to consider several questions that can help them agree on a bespoke participation strategy.

Exhibit 16: Our Ambition For Institutional DeFi

#1 What is our ambition for Institutional DeFi?

Our co-authors set and share clear ambitions to evolve their business with new technologies over long-term time horizons.

- DBS makes significant technology spending each year which includes experimentation of blockchain technology, as it prepares for a disrupted future where “blockchain will power world’s back office in five to 10 years”

- J.P. Morgan started its efforts in the blockchain and digital asset space in 2015, launched its blockchain focused business Onyx by J.P. Morgan in 2020, and is committed to investing further in the space as it plans to “bring trillions of dollars of assets into DeFi”

- SBI established its digital asset arm in 2018, set up its Capital Markets Services subsidiary in 2020, and plans to launch an institutional-grade digital asset securities platform

#2 Where and how will we participate? What will we not do?

Our co-authors continuously assess end-to-end business flow to identify where DeFi logic could potentially fit in, whether that is in their non-core functions or core functions. Formulating a firm’s participation strategy requires an understanding of their clients’ starting point, including their DeFi IQ and willingness to use new technologies. Sell-side firms could guide clients through the adoption journey from a solution-driven perspective, which includes thoroughly understanding clients’ pain points, replicating traditional offerings in a new digital format, and building tooling to assist smooth adoption while also testing innovative new products, like intra-day liquidity, and new business models, such as automated market making.

The quality of the new offerings is critical to win the confidence from end-clients. Firms can consider taking gradual approaches to focus on products that are not overly complex and/or markets requiring efficiency improvement on day one, such as illiquid asset classes.

Our co-authors are taking different approaches to participate where they see opportunities to better support end clients:

- DBS offers end-to-end capabilities in the digital assets space. DBS Digital Exchange allows for listing and trading of both digital payment tokens, including crypto and security tokens such as DBS Digital Bond originated by DBS Capital Markets; DBS Digital Asset Custody provides an institutional-grade solution to safekeep digital assets; Partior (a joint venture with Onyx by J.P. Morgan and Temasek) enables atomic settlement of payment transactions.

- J.P. Morgan provides different products and infrastructure in the space, including intraday repo and tokenized collateral services on its Onyx Digital Assets platform, and blockchain-based deposit account products on the JPM Coin System, and continues to explore expanding to other asset types and the other blockchain environments, including public blockchain.

- SBI is actively involved in the space, launching efforts across numerous digital asset classes, including NFTs, Web3 tokens, and tokenized traditional securities, and providing infrastructure and tools, such as AsiaNext, their regulated digital asset exchange joint venture with Swiss Digital Exchange (SDX).

Each finance industry institution needs to tailor their participation strategy for specific markets, business, and clients.

There are a number of “make it happen” areas firms could consider as they work to fulfill their ambitions. In this section we focus on three areas of capabilities. The degree of effort in each requires clear alignment with a firm’s ambition.

Design organizational structure to

deliver on the ambition

The level of organizational support and engagement determines the feasibility of achieving such transformative opportunities. Each of our co-authors has opted for different operational set ups, with varying extents of centralization, such as focusing on one business unit only, or stretching across the entire business. SBI Holdings created a separate centralized entity, SBI Digital Asset Holdings; JP Morgan established Onyx by J.P. Morgan within the firm to engage on blockchain matters across the entirety of the firm’s businesses; DBS leverages an ecosystem approach to engage in blockchain initiatives across the organization and externally with industry partners. DBS established DBS Finnovation, a holding company which houses DBS Digital Exchange and Partior (a joint venture among DBS, Onyx by J.P. Morgan, and Temasek).

Choose the right delivery model given

internal capabilities, risk appetite

There are a number of factors to consider when determining the delivery approach, such as ensuring that proofs of concept are done with scaling in mind; working with like-minded partners to build, test, and evolve the proposition based on lessons learned; and taking a co-creative approach with clients and regulators, being clear on what is needed from regulators to make pilots a scalable reality. External collaborations would require due diligence to ensure suitability of partners and alignment on new solution.

Regarding ways of working with partners, there is no one size that fits all. We observe a few notable delivery approaches depending on a firm’s level of belief and participation strategy – in-house builds, use of vendors, or leveraging industry consortiums. For instance, Vanguard partnered with vendor Symbiont and its blockchain platform Assembly; BNY Mellon, Morgan Stanley, and UBS joined a consortium led by iCapital to leverage blockchain-based solutions; J.P. Morgan delivered its blockchain solutions through internal efforts spearheaded by its Onyx by J.P. Morgan unit and predecessor teams; DBS leverages a mixture of options such as tapping internal capabilities for the solutioning in this pilot while also engaging external vendors for some of the other initiatives.

Develop the right talent strategy to

build propositions

Building out these bespoke solutions requires a mix of talent, not just technologists. Our co-authors have built teams with professionals from a variety of backgrounds while at the same time working to right-skill their existing teams. The co-authors note that to attract the right talent, firms need to complement talent strategies with branding efforts to ensure they have a compelling “digital brand” aligned with their ambitions. At the same time, existing talent needs to be refreshed with internal “mindset change” efforts, such as training and incentive programs.

To help drive change, we also observe peers building specialist task forces. These teams play a role in driving proofs of concept and also act as a catalyst for reshaping the culture and right-skilling teams. The task forces tend to play various roles depending on a firm’s ambition. They also can work with relevant middle- and back-office teams to understand requirements and assess new solutions, such as digital identity solutions. They also can work with front-office teams to assess demands from clients and jointly determine whether new solutions are sufficiently valuable for clients. These task forces can be complemented by other efforts depending on a firm’s starting point, including driving firmwide education initiatives, running or supporting hackathons and other internal accelerators, and driving co-creation workshops to apply DeFi and identify challenges that need to be worked through.

This joint report would not have been possible without ideas and contributions from numerous members across Oliver Wyman, DBS, Onyx by J.P. Morgan and SBI Digital Asset Holdings, and inputs from the Monetary Authority of Singapore across interviews and workshops. The co-authors would like to express deep gratitude to the following individuals: