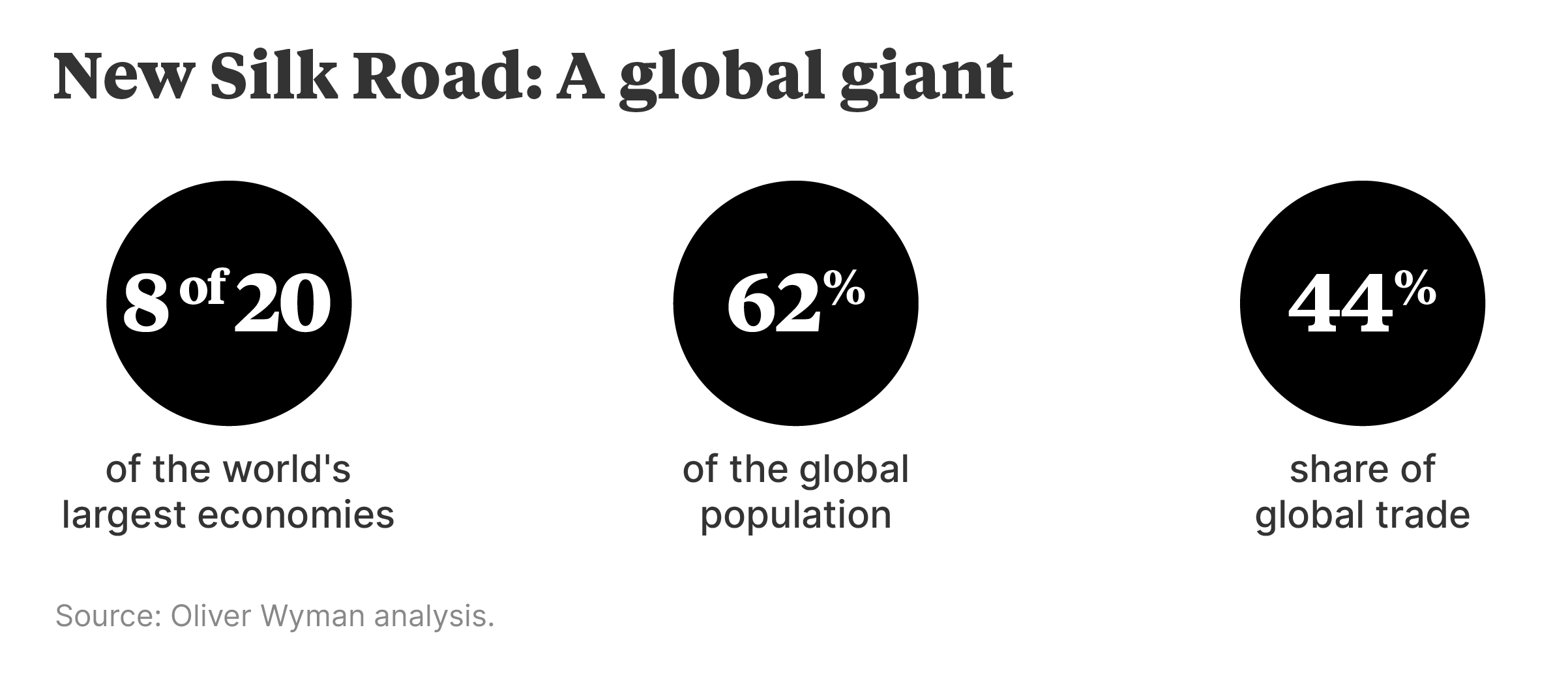

In a global economy that continues to fragment, one region stands out for its eagerness to grow closer together: the new Silk Road that links Middle Eastern countries with the economic powerhouses of Asia.

Activity along this centuries-old trade route has been supercharged over the past decade by the region‘s strong economic growth, deep capital pools, and the growing purchasing power of its 4.9 billion people. The area accounts for 40% of global GDP and is on track to reach nearly 50% by 2040.

Secular trends like the clean energy transition are strengthening exchanges between regional economies. Even challenges like supply-chain disruption and US-China relations are tending to reinforce bonds as Chinese firms pivot toward other Asian countries and the Middle East.

The region’s wealth and dynamism present opportunities that companies around the world can’t afford to ignore, according to a recent report by Oliver Wyman.

Companies should focus on specific corridors of activity along the Silk Road, such as manufacturing supply chains linking China with countries like Vietnam, Malaysia, and Indonesia, or private wealth management business revolving around regional hubs like Hong Kong, Singapore, and Dubai. They can look to align with national development priorities that promote specific industries and try to identify the right partner, such as a global or regional player with interests in multiple countries. Companies also should look to nurture talent with experience in both Asia and the Middle East.

Many factors are driving growth and deeper integration along the Silk Road, but three stand out: supply-chain adjustments, the transition to clean energy, and accelerating digital disruption.

Diversifying supply chains within Asia

Commerce in the region has grown tremendously in scale and sophistication since the turn of the century, when exchanges of Gulf oil and gas and Chinese consumer goods dominated activity.

Today Silk Road countries account for 86% of global exports of semiconductors, more than 70% of phones and computers, and 40% of oil. While many companies have looked to source production closer to home or in friendly countries to de-risk supply chains in response to pandemic disruptions and US-China trade tensions, much of the realignment is taking place along the Silk Road itself, particularly in economies that have opened up to foreign investment.

Vietnam is the major winner so far, increasing its share of global consumer goods exports by more than a third in the past five years across everything from electronic components and smartphones to athletic footwear. India also is scoring some notable gains. Apple and its suppliers have accelerated the growth of production capacity in India to reduce their dependence on China. They now make an estimated 7% of iPhones in the country, and reportedly aim to increase that share to around 25% within three years.

China will remain the world’s largest manufacturer but increasingly invest across the region, particularly in Gulf economies where governments are focused on strengthening domestic manufacturing. Such investments are supported by closer policy connections. Asia is home to two of the world’s three largest free trade areas — the Regional Comprehensive Economic Partnership and the Comprehensive and Progressive Agreement for Trans-Pacific Partnership. Middle Eastern countries are looking to plug into those networks. The United Arab Emirates has signed trade and investment agreements with India and Indonesia, is pursuing a similar pact with Vietnam, and gained observer status with the 10-country Association of Southeast Asian Nations.

Clean energy symbiosis

While oil and gas remain essential lubricants of economic ties along the Silk Road, clean energy technology is becoming an increasing priority. Middle Eastern countries are looking to position their economies for a post-oil future and have a big appetite for technology and minerals that China is happy to supply.

Chinese electric vehicle (EV) and battery companies have tripled their exports to the Silk Road region in the past three years and are making investments in the region. China’s Skyworth agreed last year to build an EV battery factory in Turkey. South Korean steelmaker POSCO, meanwhile, is developing a green hydrogen plant in Oman and Japan’s JERA recently signed a memorandum of understanding to explore green hydrogen projects with Saudi Arabia’s Public Investment Fund (PIF).

Capital also is flowing the other way, providing timely financial support for Chinese EV makers in the midst of a price war. CYVN Holdings, an Abu Dhabi-owned smart mobility fund, agreed in December to invest $2.2 billion to raise its stake in Chinese EV maker Nio to 20%. And in February, Nio signed a deal to license technology to CYVN’s EV subsidiary.

Riding the digital highways

One of the strongest vectors driving closer economic integration along the New Silk Road is the digital economy. The region is home to 1.1 billion people between the ages of 15 and 29, most of whom grew up using the internet. That helps explain why five of the world’s top 10 gaming companies are based in the region. And 70% of the region’s employees, on average, use generative artificial intelligence at least once a week, according to surveys by the Oliver Wyman Forum.

Saudi Arabia’s PIF recently became the largest outside shareholder in Nintendo and invested $265 million in the Chinese eSports company VSPO. Chinese gaming leaders NetEase and Tencent are investing in mobile opportunities in the Gulf and Southeast Asia, and tapping regional talent from Egypt to India. And Chinese autonomous driving group Pony.ai recently raised $100 million from Neom Investment Fund, the Saudi sovereign fund supporting the futuristic high-tech development in the country’s northwest, and agreed to establish a regional research and development and manufacturing headquarters in Saudi Arabia.

Silk Road economies are building for the future, and deepening the flow of goods and services, capital, and human talent. That dynamism offers opportunity to a world in need of a growth stimulus.

The global aircraft industry has finally recovered from the disruption of the pandemic, but the new growth trajectory looks more moderate, and potentially bumpier, than what was envisaged only a few years ago.

The world’s commercial aircraft fleet expanded to 28,400 planes at the start of this year, eclipsing the previous high set in January 2020, according to Oliver Wyman’s latest global fleet forecast. It projects the fleet will grow at a compound annual rate of 2.5% over the coming decade, considerably slower than the pre-pandemic period. In early 2020, Oliver Wyman predicted the fleet would top 39,000 aircraft by 2030. Now we don’t see the industry hitting that level until 2036. In essence, aircraft manufacturers have lost six years of growth.

It’s not for lack of demand. Passenger traffic hit a new high in the United States last year and is on track to set a global record of 4.7 billion this year. But Airbus and Boeing, as well as their suppliers, are bumping up against the limits of their production capacity.

The two global aircraft manufacturers aim to boost output over the coming decade, but both failed to reach their targets in 2023 – and they may continue to do so without significant investment in their own and suppliers’ production facilities. The industry also suffers from a shortage of skilled labor.

Additionally, engine makers are struggling to get their latest models in the air. Manufacturers have experienced problems and delays with next-generation engines, including potential quality control problems with Pratt & Whitney’s geared turbofan platform. That prompted regulators to order inspections that grounded hundreds of aircraft recently.

India throttles up

Meanwhile, another transition is underway with India overtaking China as the fastest-growing market for new planes.

Over the last 12 months, Indian airlines have placed orders for more than 1,800 aircraft, and the nation’s fleet is expected to grow to two and a half times its current size of 600 planes by 2034. Only 3% of the Indian population flies regularly, but with 1.4 billion people — the world’s largest population — and a robust economy projected to grow at a 6.5% rate this year and next, demand for air travel is taking off.

In China, by contrast, a property-driven economic slowdown has cooled the growth outlook. Yet this is a vast market and the country’s airlines are expected to take delivery of 4,200 aircraft over the coming decade. That would see China overtake Western Europe with the world’s second-largest fleet, behind North America.

CEO of Hong Kong transit operator MTR Corp.

“People may be surprised that with a reasonably moderate investment, they can get significant improvement in terms of environmental focus. That’s the kind of area where we're investing.”